SEC Signals Next Phase of Executive Compensation Disclosure Reform

Spring 2026 Regulatory Agenda Places Item 402 Simplification on the Rulemaking Calendar

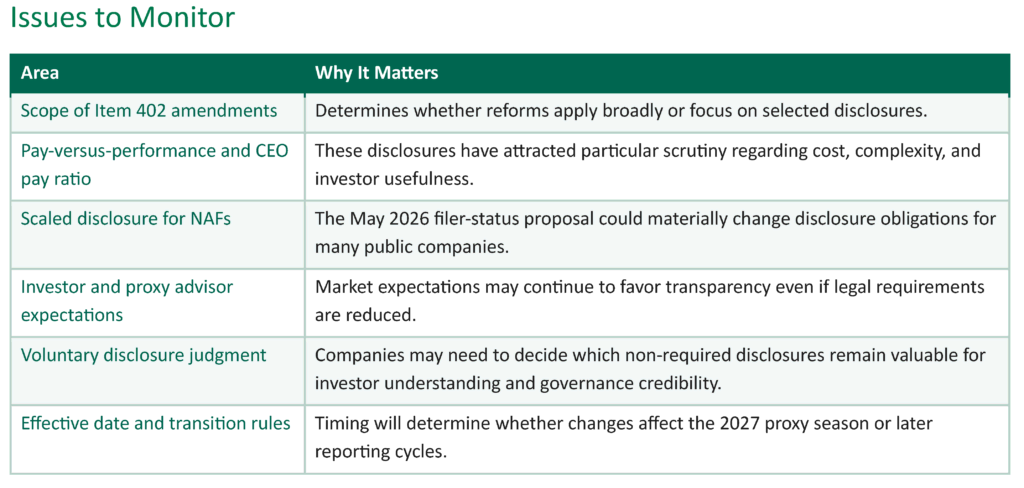

KEY TAKEAWAYS

- Executive compensation disclosure reform is now on the SEC’s recently released Spring 2026 rulemaking agenda.

- Roundtable recommendations provide an early roadmap for potential reform.

- This appears to be the next phase of the SEC’s broader simplification effort.

- No disclosure changes are effective today.

- Simplification should mean better disclosure, not just less disclosure.

Spring Regulatory Agenda Signals a Direct Focus on Compensation Disclosure

The SEC’s Spring 2026 Regulatory Flexibility Agenda (Reg Flex Agenda) was released as part of the Federal 2026 Regulatory Plan and Unified Agenda that the Office of Information and Regulatory Affairs (OIRA) made public on July 3, 2026. The agenda includes an Executive Compensation Disclosure Reform initiative focused on rationalizing Item 402 disclosure requirements.

Builds on Earlier SEC Simplification Proposals

The agenda follows the May 2026 proposal expanding scaled disclosure eligibility for many non-accelerated filers.

Recent SEC Commentary and Roundtable Recommendations Provide Useful Context

Key recommendations discussed following the June 2025 Roundtable include:

- Refocusing the Compensation, Discussion, and Analysis (CD&A) on principles-based disclosure that is material to shareholders and encouraging the relocation of boilerplate disclosure that does not change year-to-year to the companies’ website.

- Replacing three equity award tables (Grants of Plan-Based Awards, Equity Awards Outstanding at Year-End, and Options Exercised and Stock Vested) with a new single Equity and Cash Incentive Award Activity Table.

- Limiting Pension Benefits Table disclosure to companies with active pension plans.

- Revising CEO Pay Ratio calculations to use U.S. employees only.

- Simplifying Pay-Versus-Performance disclosure to focus on CEO/PEO compensation only and eliminating the Company Disclosed Measure, U.S. GAAP Net Income, list of most important performance measures, and the comparison of Compensation Actually Paid to performance, whether in graphic or narrative form.

- Increasing perquisite disclosure thresholds and indexing them for inflation.

- Treating executive security costs as a business expense rather than a perquisite where appropriate

Based on Chairman Atkins’ prepared comments at the Society for Corporate Governance’s National Conference on July 9, 2026, we expect the proposed revisions will place a strong emphasis on simplification, materiality, and the reassessment of the existing rules through a holistic lens that should benefit Large Accelerated Filers.

What Companies Should Do Now

Monitor rulemaking developments and evaluate which disclosures remain useful to investors even if requirements are reduced. Consider sending the SEC a comment letter with recommended changes to clarify and streamline the executive compensation disclosure rules either before or after the SEC issues the proposed rule change.