What 2025 ISS Say on Pay Opposition May Signal for the 2026 Season

In 2025, Institutional Shareholder Services (ISS) opposed 10% of S&P 500 company Say on Pay (SOP) proposals. This was consistent with ISS’s historical average “against” rate from the previous five years (2020 through 2024). In this Viewpoint, we explore the ISS quantitative pay-for-performance (P4P) outcomes and the qualitative rationale provided by ISS for SOP opposition for S&P 500 companies in 2025. We also look ahead to what the findings may signal for the 2026 SOP season.

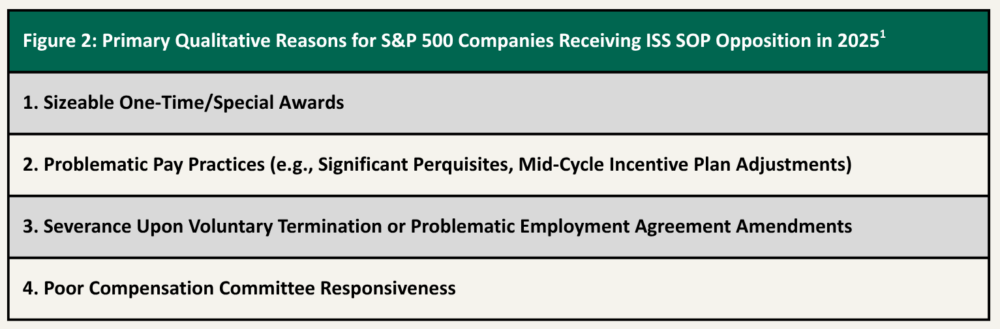

In general, in 2025, companies demonstrated strong alignment on ISS’s quantitative P4P tests (and particularly on the Relative Degree of Alignment (RDA) assessment that compares relative CEO pay to relative total shareholder return (TSR)). Therefore, ISS’s qualitative review, in which it scrutinizes compensation design and governance practices, drove much of ISS’s 2025 SOP opposition. Specifically, ISS flagged companies for using special awards and providing severance benefits for voluntary separation, as well as other practices it views as problematic.

1. Strong Quantitative P4P Results

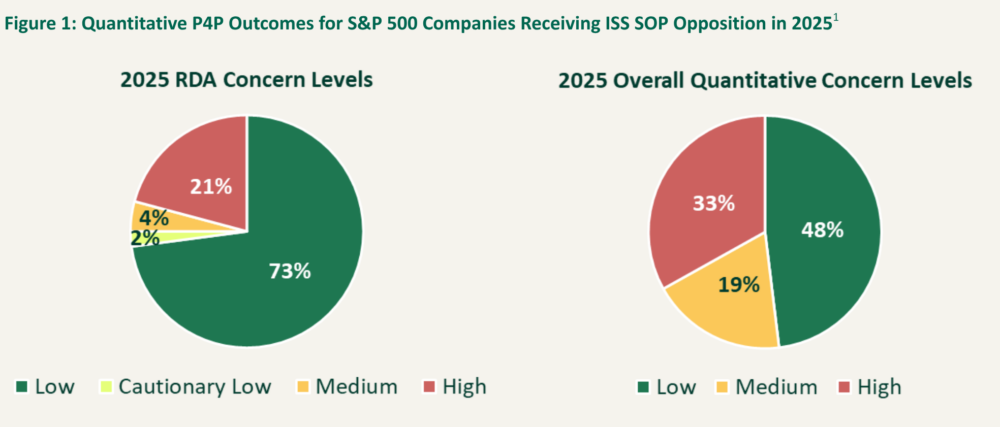

ISS quantitative P4P test results have historically been a reliable predictor of an ISS “against” SOP recommendation. However, in 2025, we observed strong quantitative P4P results for companies receiving opposition from ISS on SOP, suggesting quantitative factors played a smaller role in ISS opposition.

As shown in Figure 1, in 2025, 73% of S&P 500 companies that received an “against” SOP recommendation from ISS scored “low” concern on the primary RDA test. In other words, the majority of S&P 500 companies opposed by ISS on SOP demonstrated alignment between CEO pay and TSR relative to ISS-defined peers. Further, nearly half of S&P 500 companies (48%) received an overall “low” concern when incorporating the other quantitative P4P tests.

2. ISS Qualitative Concerns Centered on Unconventional Pay Actions

Among S&P 500 companies receiving ISS SOP opposition in 2025, the top three areas of ISS criticism within its qualitative review were related to the use of non-standard pay elements, such as special awards, high-value security benefits, and severance payments for voluntary separation. Additionally, for companies who experienced low shareholder SOP support last year, ISS continues to suggest that companies take meaningful measures to engage with investors and provide thoughtful, clear disclosure around actions taken to address prior shareholder concerns.

Predictions for the 2026 Say on Pay Season

Looking ahead, ISS’s evolving policy framework for 2026 introduces several changes that could impact SOP outcomes this season.

- Despite recent strong quantitative P4P outcomes, turmoil may lie ahead. ISS lengthened the timeframes for the primary quantitative tests in 2026, which may lead to unexpected P4P concern levels. The RDA time period increased from 3 years to 5 years, and the Multiple of Median (MOM) time period increased from a single 1-year period to an average of a 1-year period and a 3-year average period. For companies that demonstrated recent strong P4P alignment, concern levels could be elevated by the longer lookback periods for pay and performance, and vice versa. The extended time period also means that one-time awards will be included in these calculations longer, potentially raising ISS’s concern levels for RDA and MOM.

- For 2026, ISS also adopted a policy that signals greater openness to high-value security benefits if reasonable rationale is disclosed. We anticipate an increase in the prevalence of executive perquisites and security-related benefits, as well as an improvement in the quality of disclosure for these benefits this proxy season.

- Further, ISS updated its 2026 policy to consider extended time‑vested awards as a structural program feature that, like long-term incentive programs that are majority-weighted toward performance‑based equity, can help mitigate P4P concerns. It remains to be seen whether this policy change will influence design change, as many investors continue to expect long-term performance-based equity to be a significant component of executive compensation[2].

These 2026 ISS policy updates, combined with observations from 2025, demonstrate that while the proxy advisor and SOP landscape continues to evolve, the importance of thoughtful program design and robust disclosure remains constant.

General questions about this Viewpoint can be directed to Linda Pappas (linda.pappas@paygovernance.com).

___________________

1 Reflect ISS SOP vote recommendations available through December 31, 2025, collected from ISS Corporate’s Voting Analytics database.

2 Ira T. Kay, Linda Pappas and Lane T. Ringlee. Are Institutional Investor Preferences for Performance-Based Equity Really Diminishing in Favor of Time-Based Shares? Pay Governance. August 19, 2025. https://www.paygovernance.com/resource/are-institutional-investor-preferences-for-performance-based-equity-really-diminishing-in-favor-of-time-based-shares