Board of Directors Compensation: Past, Present and Future

Introduction

There has been a massive shift in how outside Board Directors have been paid over the past 20 years. This has largely been fueled by changes in corporate governance practices over time. Overall, the shift has been away from paying Directors like executives and towards paying outside experts for their time and contributions during their term of service.

Historical Context

Twenty years ago, the Director pay model at a large corporation often had the following features:

- directors were commonly eligible for certain benefits programs and pensions;

- vesting schedules for equity awards were 3 or 4 years long, similar to those for executives;

- equity awards were in the form of stock option grants (also used for executives), and Director awards were expressed as a number of shares rather than a grant value;

- many companies did not differentiate pay for Committee service; and

- Lead Director roles and Director stock ownership guidelines were absent.

Although some changes were caused by market conditions, we believe most of the changes to Board pay over the past 2 decades were driven by the following 6 governance-oriented drivers:1

1.1996 NACD Blue Ribbon Commission Report on Director Professionalism ” This was a very influential report covering recommended roles and responsibilities of the Board. It included strong recommendations to pay Directors via cash and equity and to dismantle Director pension and benefits programs because they created too much alignment with the existing senior management team. It was also an early proponent of having an independent Director in charge of certain Board activities, eventually leading to the rise in prevalence of Lead Director roles.

Within a few years of its publication, most major companies had eliminated/frozen Director pensions and significantly reduced Director benefits, putting more emphasis into equity-based compensation.

2. Sarbanes Oxley (SOX) ” SOX, effective in 2002, came out on the heels of the Enron scandal and multiple stock option “back-dating” scandals. It reframed the Board’s responsibilities and included an expanded role for its Audit Committee.

SOX influenced several changes. It led to an understanding that the Director role would be more time consuming and subject to more scrutiny, which led to higher Director pay to recognize expanded time requirements. It caused more differentiation in pay by Committee, with premiums paid to the Audit Committee members and Chairs, who had expanded duties under SOX. Following SOX, and the various scandals that led to it, the majority of companies shifted from using stock options to using full value shares for Director equity grants.

3. Elimination of Staggered Board Elections ” In the past, the majority of companies had staggered Board elections: 60% as of 2002, according to one study. A typical staggered term structure had 3-year terms for each Director, with about one-third of Directors up for election annually. There were several reasons for the popularity of staggered terms, including a desire to increase stability and have a form of takeover defense in place. Shareholders and governance organizations engaged in a multi-year campaign for annual elections, which allowed shareholders to vote on the full slate of Directors every year. The vast majority of companies now have annual elections for the full Board: less than one-third of the S&P 500 companies still have staggered Boards today.1

A 1-year Board term led to a compressing of Director equity vesting schedules so that vesting is completed by the end of the Board term. When Directors had 3-year terms, equity vesting of 3 years (or longer) was more common, matching equity vesting schedules used for executives.

4. Recent Focus on Board Replenishment ” Especially in the past 5 years, there has been increasing shareholder and governance organization focus on Board replenishment with the idea that more frequent Director changeovers could promote enhanced diversity, add new ideas and specialties, and potentially benefit Director independence.

This is another factor leading to shorter vesting schedules for equity awards, eliminating any economic obstacles to Director retirement. It has also led to the heightened importance of ensuring that competitive packages assist in recruiting highly-qualified candidates.

5. Separation of CEO and Board Chair ” Over the past 20 years, corporate governance organizations and some shareholder activists have pushed for the separation of the Chair and the CEO roles. In the past, most U.S. companies had CEOs in both roles; this is different from typical practice in other countries such as the U.K., where the roles are separate. There has been a significant uptick in separate Chairs recently (44% of the S&P 500, up from 21% in 2001).2 While many companies have not separated the 2 functions, there has been a rise in the independent Lead Director role to ensure that certain Board activities are handled by an outside Board member rather than the CEO in those cases.

Lead Directors and Non-Executive Chairs have become much more common, and companies have developed additional retainers to compensate for these roles.

6. Dodd-Frank Regulation ” One of the early regulations implemented under Dodd-Frank was to have an advisory SOP vote by shareholders so they could voice their support (or lack thereof) of executive compensation programs. The first votes took place in 2011.

Managing the SOP process has added to the responsibilities of the Compensation Committee Chair position; in recent years, Compensation Committee Chair retainers have moved closer to Audit Committee Chair retainers.

How These Governance Shifts Translated to the Board Pay Model

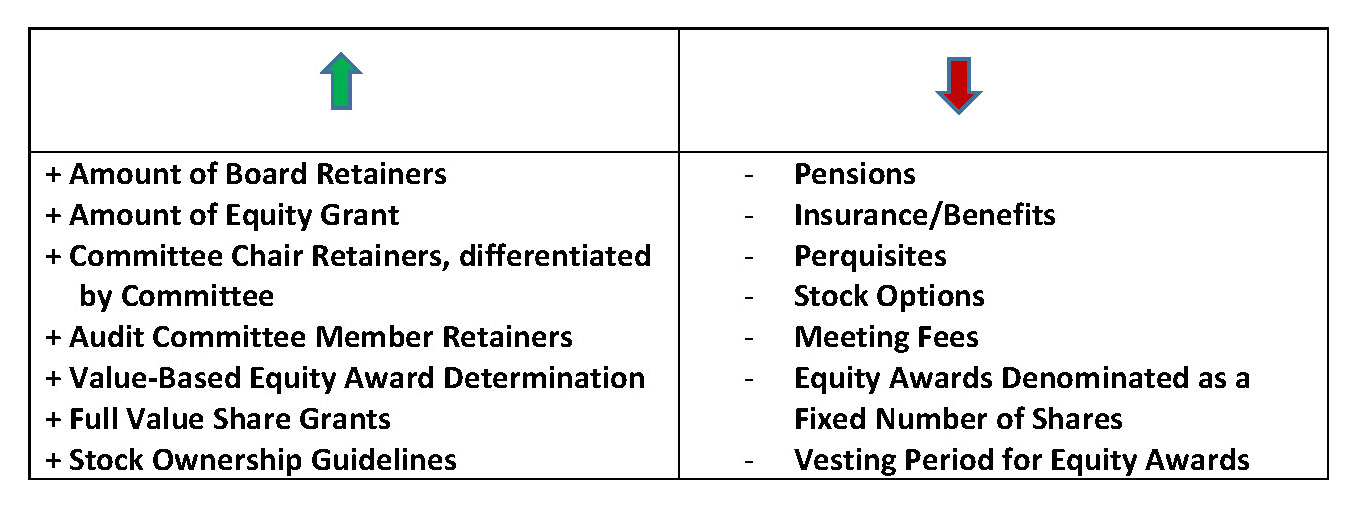

The governance shifts described above have led to major changes in the size and design of Director pay:

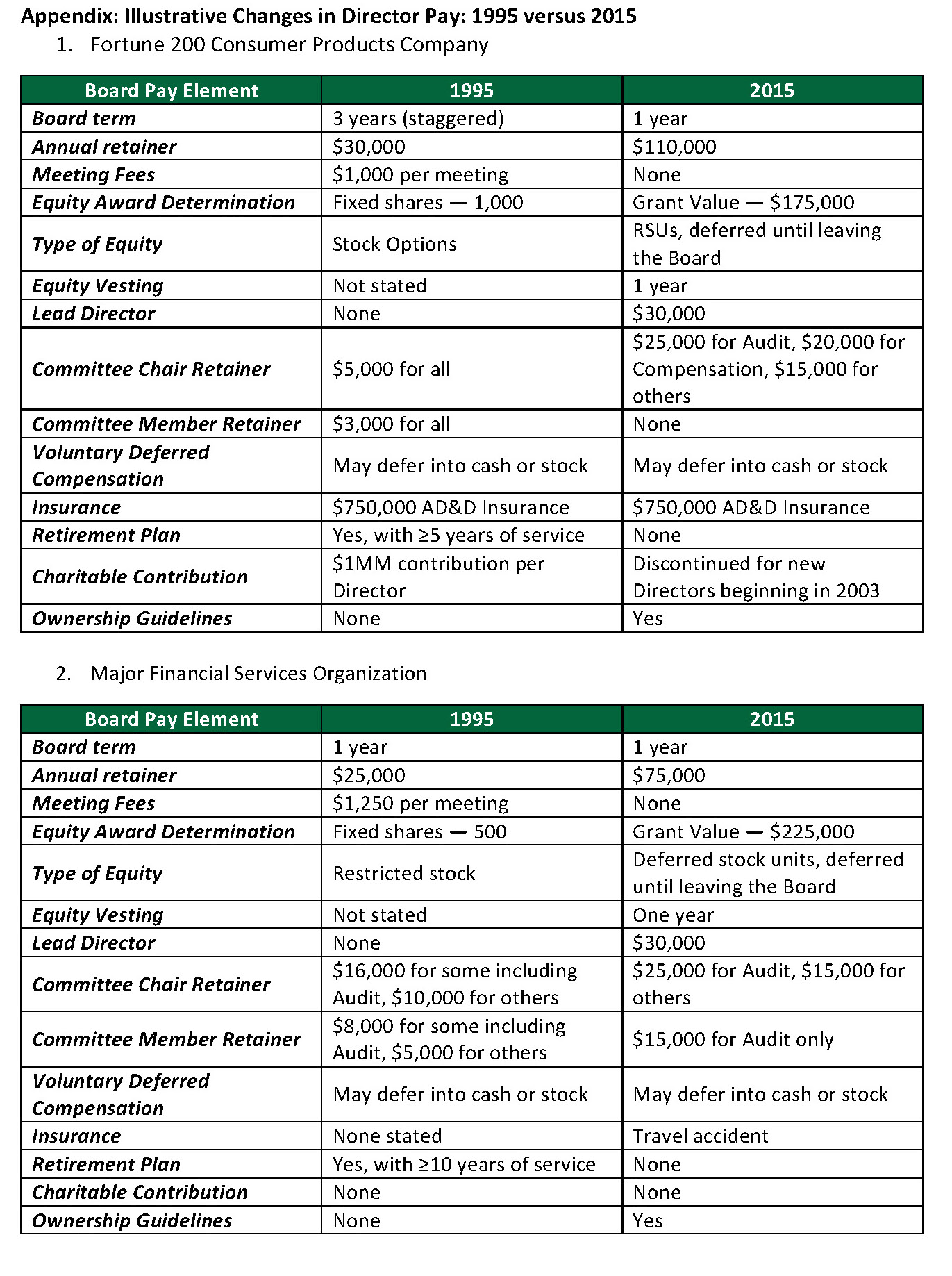

To illustrate the type and extent of the changes between 1995 and 2015, 2 specific company examples are provided in the Appendix.

Current Board Pay Status

The most common pay elements at S&P 500 companies currently are:

- cash retainers for Board service;

- annual equity grants for Board service;

- Committee Chair retainers; and

- Lead Director or Non-Executive Chair Retainers.

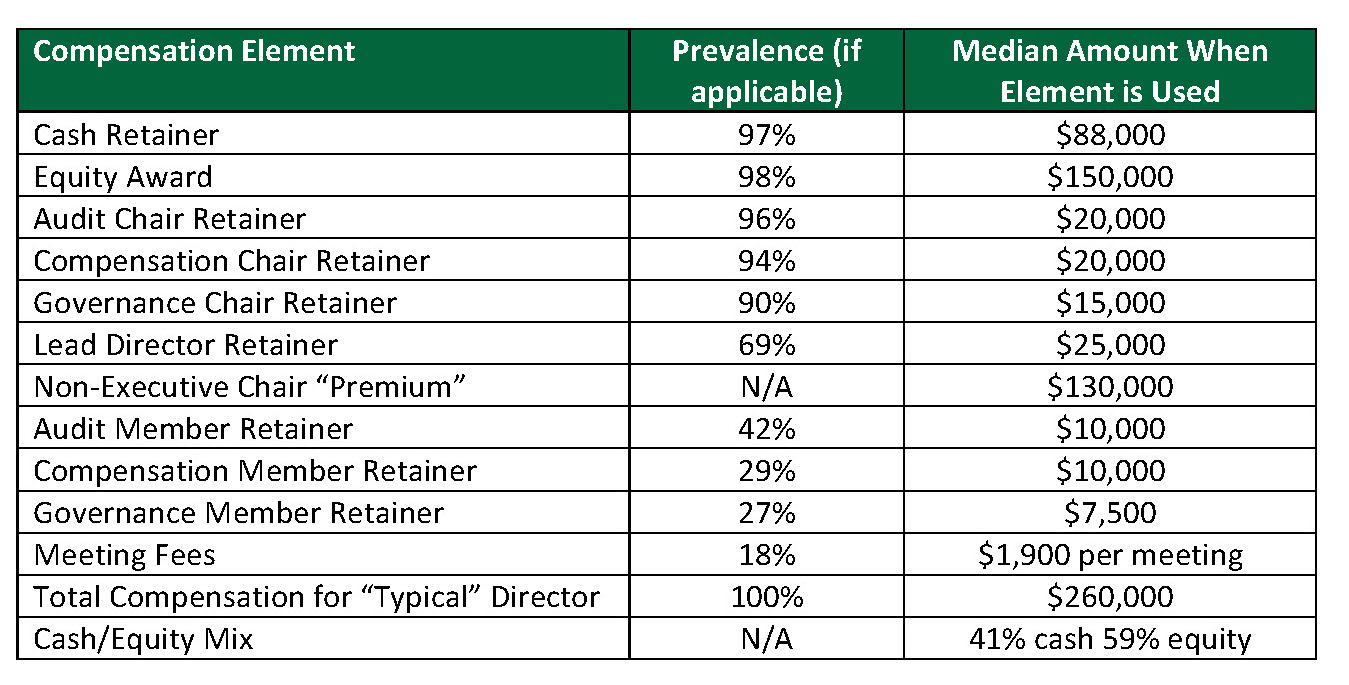

Within the S&P 500, some companies pay non-Chair Committee members a retainer; a minority still pay meeting fees. Director stock ownership guidelines are common, as are voluntary deferred compensation programs to defer into cash or stock. Perquisites are relatively limited but still in use. The following table presents 2015 prevalence statistics and median pay amounts for S&P 500 companies:

Director pay levels tend to be very closely clustered together, unlike the wider distribution of executive pay. For example, the 25th percentile of total compensation for the S&P 500 sample is $230,000, and the 75th percentile is $295,000 compared to a median of $260,000. This means the vast majority of S&P 500 companies pay Directors within $35,000 of the median (a relatively narrow range of ¬±15%). Because Director pay data is so tightly clustered, it is useful to consider dollar variance values from the median ” not just percentile ranking ” when considering pay competitiveness.

Current Design Considerations

Although much of Board pay is very homogenous across companies, there are some design questions which arise and should be addressed when reviewing the design of a company’s Board pay package.

How should non-Chair Committee service be recognized?

When meeting fees were common, they provided a way for Directors to recognize Committee member service. While almost all companies pay a retainer to the Committee Chair, some do not have Committee member retainers. In the absence of either Committee member retainers or meeting fees, a Director serving on multiple Committees receives the same pay as a Director serving on a single Committee. Some Boards prefer a non-differentiated package (eg, if the Board has an “open door” policy and Directors routinely attend Committee meetings even though they are not members). However, for some companies, paying all Directors the same amount despite different Committee involvement is seen as unfair. It is important to determine whether Committee time should be differentiated and by how much.

How to handle a Committee with an unusually high number of meetings in a given year

This is another area which is complicated by the elimination of meeting fees. What do you do if, due to some unforeseen circumstance such as an acquisition or crisis, a Committee has an unusual high number of meetings in a given year? When the number of meetings rises above 20 for the year, the regular Director package may be insufficient for the vastly-expanded time demands. One way to handle this situation is to create a special retainer, but these can be difficult to explain. Further, it can be hard to establish a clear standard for when the company will or will not pay a special retainer. A potentially simple approach would be to establish a Committee retainer, which covers up to a specific number of meetings (perhaps 10) in a given calendar year. If there are more meetings than that, the company begins to pay a per-meeting fee. It is better to decide in advance how best to deal with a high volume of Committee meetings rather than trying to design a stop-gap in the middle of a challenging Committee year.

How to offer deferred compensation

Many companies, especially those in the S&P 500, allow Directors to defer cash retainers; many also grant deferred stock units, which Directors receive after they leave the Board. While both practices are competitive and can be an attractive part of the package to Directors, it is important for company management to consider how many deferral choices can be reasonably administered. Should Directors get the entire deferred amount in a lump sum the year they leave the Board? Can Directors elect to take deferred balances in installments over 5 or 10 years? More choice is attractive for Directors, but it is important to consider how much the company can affordably administer. This issue is particularly true for small- and mid-cap companies with leaner in-house resources.

Another item related to deferred compensation is mandatory equity deferral programs, where equity awards are automatically deferred until Directors leave the Board. This type of design can be very beneficial, and it eliminates potential concerns over Director insiders selling stock to cover tax costs while on the Board. However, there can be very large differences in age and wealth across a group of Directors: large mandatory deferrals may be attractive for some and less attractive to others. It is important to make sure all Directors understand the economics and ramifications of mandatory deferrals and agree on the design before implementation, since it is almost impossible to change the deferrals once they are in place.

Recent Emerging Issues

A recent litigation decision has further reinforced the importance of having a clear process for making Director pay decisions ” including having specific Director equity grant limits” in place to reduce exposure to lawsuits on Director pay. This topic garnered much attention after a recent Delaware Chancery Court ruling (Calma vs Templeton): the Court refused to apply the business judgment rule to dismiss claims against Directors who received large restricted stock awards.

- The Court decision was driven by the fact that Directors approve their own compensation, that there were only generic individual equity award limits in place in the equity plan (ie, the limit applied to all plan participants and was not specific to Directors), and that the limit was seen as not “meaningful.”

- Following this decision, companies started reviewing their Director equity plans, and many have filed meaningful equity limits for shareholder approval. These limits are best set as a dollar amount. In addition, as a result of this ruling and the desire to reduce exposure to litigation, certain other practices are being considered on a company-by-company basis:

– having a standalone Director Equity Plan rather than combining it with the Executive Plan;

– considering cash (or total) compensation limits, even though the focus of the lawsuit was on equity awards;

– ensuring that an appropriate and robust process is in place for determining Director pay competitiveness; and

– providing expanded disclosure of the pay-setting process in the annual proxy.

Across the S&P 500, we have seen a significant uptick in the submission of Director equity limits for shareholder approval since 2013, with limits generally in the $500,000 to $1 million range.

Predictions for the Future

While always difficult to predict, we offer these thoughts on areas which may see more attention in the next 10 years:

- Perquisites ” While many of the larger Director perquisite programs have been eliminated, certain programs are still used by some companies, including product discounts, charitable contribution matches, and spousal travel reimbursement for certain Board events. Given the current environment, it is likely that there will be continued pressure to reduce Director perquisites.

- Executive Chair Pay For Former CEOs ” As part of the succession planning process at some companies, the retiring CEO becomes Executive Chair for a few years. Compensation packages for these Executive Chairs range widely and in some cases can be as much or more than the new CEO’s. While continuity and smooth succession are important, we believe shareholder activists and proxy advisors may start paying more attention to the size of Executive Chair packages for former CEOs, particularly if such legacy pay levels continue for ‚â•1 year after retirement and do not correspond well to the level of effort exhibited by the incumbent.

- Lead Director Pay ” When the Lead Director role began, it often was unpaid. As the role has evolved, compensation is now commonly just above the level of retainer provided for the Audit Committee Chair. As this role takes on more prominence and demands more time, we expect Lead Director pay will exceed Committee Chair pay by a more significant margin.

- Relationship of Pay Premiums for Non-Executive Chairs versus Lead Directors ” Non-executive chair pay continues to be substantially higher than Lead Director pay: based on the S&P 500 data shown earlier, a Non-Executive Chair is paid about $100,000 more for the role. This pay gap between the 2 roles may be based on valid differences in role and responsibilities. However, it is not always clear to outside stakeholders what the exact roles are. As most large companies have 1 of these 2 roles in place, we expect more discussion in the future on what the premium should be for each of the 2 roles. As noted above, we believe Lead Director pay will increase, closing some of this gap.

Conclusion

Director pay is very important in recruiting and retaining highly qualified Directors. It is also symbolically important as a representation of the company’s attitudes towards corporate governance. We anticipate further changes over the next 2 decades as corporate governance continues to evolve.

____________________________________