How the COVID-19 Pandemic Influenced Incentive Plans

The COVID-19 global pandemic has had a profound impact on the economy and forced many companies to make dramatic changes in staffing, operations, supply chains, and short- and long-term business plans. At the time this article is being written, close to 10 million fewer people are employed in the U.S. than at this time last year. Many companies acted swiftly at the onset of COVID-19 in the U.S. by implementing base salary reductions, enacting furloughs, suspending 401(k) matches, and taking other measures to reduce cost, improve cash flow, and strengthen balance sheets. By the end of April 2020, as lockdowns eased, the major stock indices started to recover, and companies showed their resiliency by adapting their operations to fit the new COVID-19-dominated environment.

As companies reset business plans and priorities in response to the pandemic, compensation committees and senior management teams also began to assess the pandemic’s impact on their incentive plans ” both what had happened and what may yet happen ” and discuss what actions, if any, might be appropriate to address these disruptions in compensation programs that were established prior to the onset of the pandemic.

Pay Governance reviewed the proxy filings of S&P 1500 companies (available as of February 8, 2021) with fiscal years (FYs) ending between April 30, 2020 and October 31, 2020 (“early filers”). We focused on disclosure related to 2020 annual incentives (AIs), long-term incentives (LTIs) with performance periods ending in 2020, and “in-flight” incentive awards (i.e., incentive awards with a performance measurement period that has not yet concluded). We also reviewed forward-looking disclosures about 2021 compensation structures to identify the key changes (or lack thereof) and researched how shareholders and the proxy advisory firms reacted to the changes.

Our research revealed the following key takeaways:

- While approximately 60% of companies took some type of action for their FY 2020 or 2021 incentive plans, the majority of early filers did not make modifications to their AI or LTI plan payouts as a result of the impact of COVID-19.

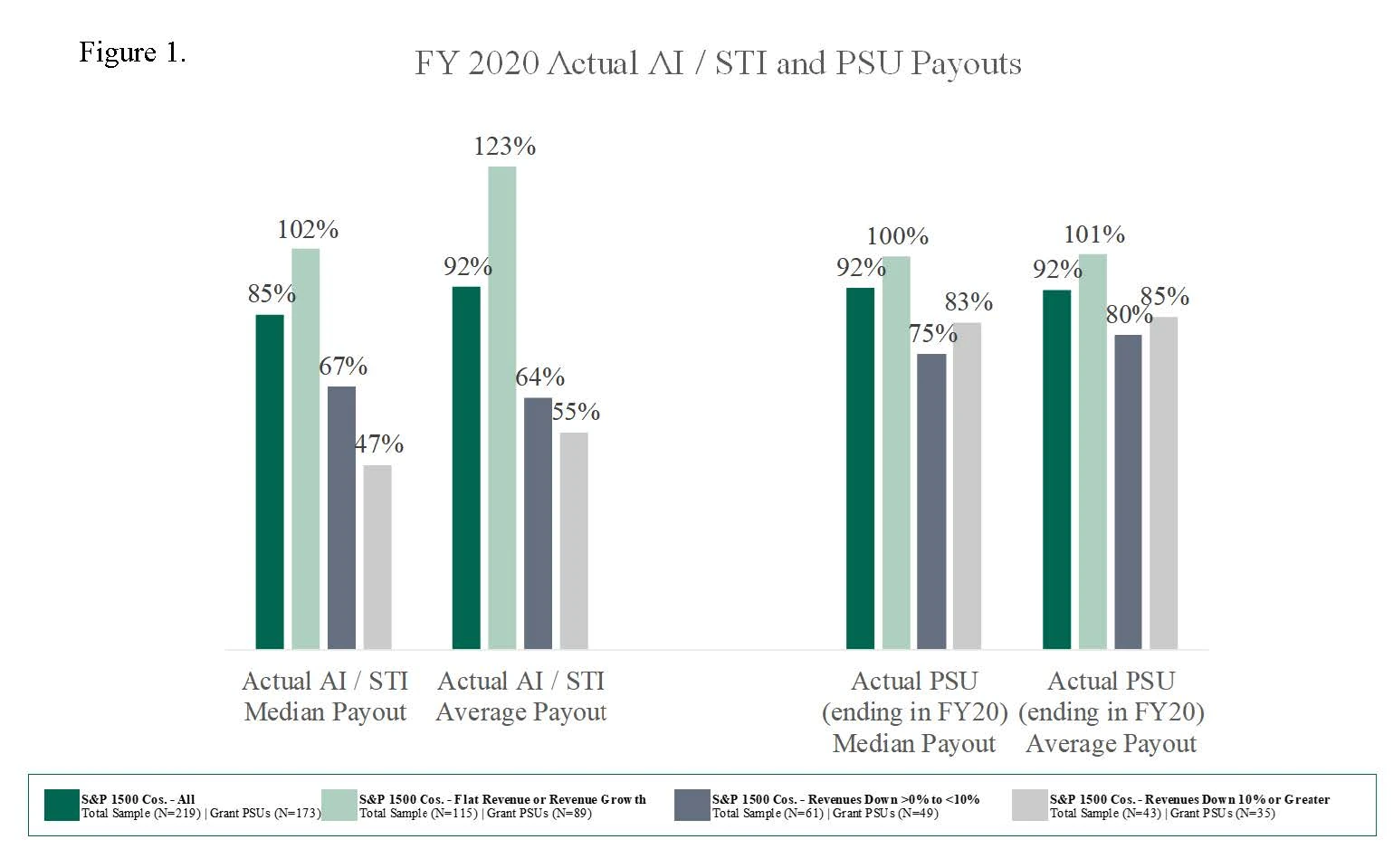

- Modifications to 2020 AI plan payouts were more common among companies hardest hit by the pandemic (defined in our analysis as companies with a revenue decline of 10% or more). Such adjustments were generally viewed as reasonable by shareholders and proxy advisory firms, as the resulting payouts remained below target and applied to all plan participants ” not just the named executive officers ” and disclosure included a sound rationale and process for making the adjustments.

- Modifications to performance share units (PSUs) with measurement periods ending in 2020, modifications to in-flight PSUs, or special/one-time LTI awards intended to offset lost PSU award value have not been well received by shareholders and proxy advisory firms as PSUs are intended to reward long-term performance.

- Prospectively disclosed changes to 2021 AI and LTI plans were most common among companies severely impacted by the pandemic. Common changes included new metrics, and, for LTI programs, increased use of time-vested restricted share units (RSUs). Companies that shifted away from performance-based LTI vehicles (e.g., adopted 100% RSUs for 2021) were more likely to receive significant criticism from the proxy advisory firms.

- FY 2020 AI and LTI payouts were noticeably lower among the hardest hit companies than other fiscal year-end filers, which suggests companies adhered to a pay-for-performance philosophy.

- Institutional Shareholder Services (ISS) and Glass Lewis recommended “FOR” Say on Pay in the same proportion for companies that adjusted incentives and those that did not adjust incentives.

The insights and data gathered from these “early filers” are not prescriptive, but rather one of several reference points for companies to consider as they determine go-forward annual and long-term incentive designs and draft CD&A disclosure related to changes that have already been approved/implemented.

Summary Findings

Approximately 60% of early filers took some type of action for their FY 2020 or 2021 incentive plans. These actions included modifications to 2020 AI plan payouts based on discretion and revised 2021 long-term performance plan designs.

When we adjusted for business impact (as measured by changes in revenue), those companies that were more severely impacted were more likely to have made:

- Adjustments to 2020 AI payouts;

- Changes to AI design for 2021; and

- Changes to LTI plans for 2021.

As Figure 1 below indicates, 2020 AI and PSU payouts (for cycles ending in 2020) tracked closely with business impact, as those companies with year-over-year revenue decreases in their last two fiscal quarters had noticeably lower incentive payouts as a percentage of target.

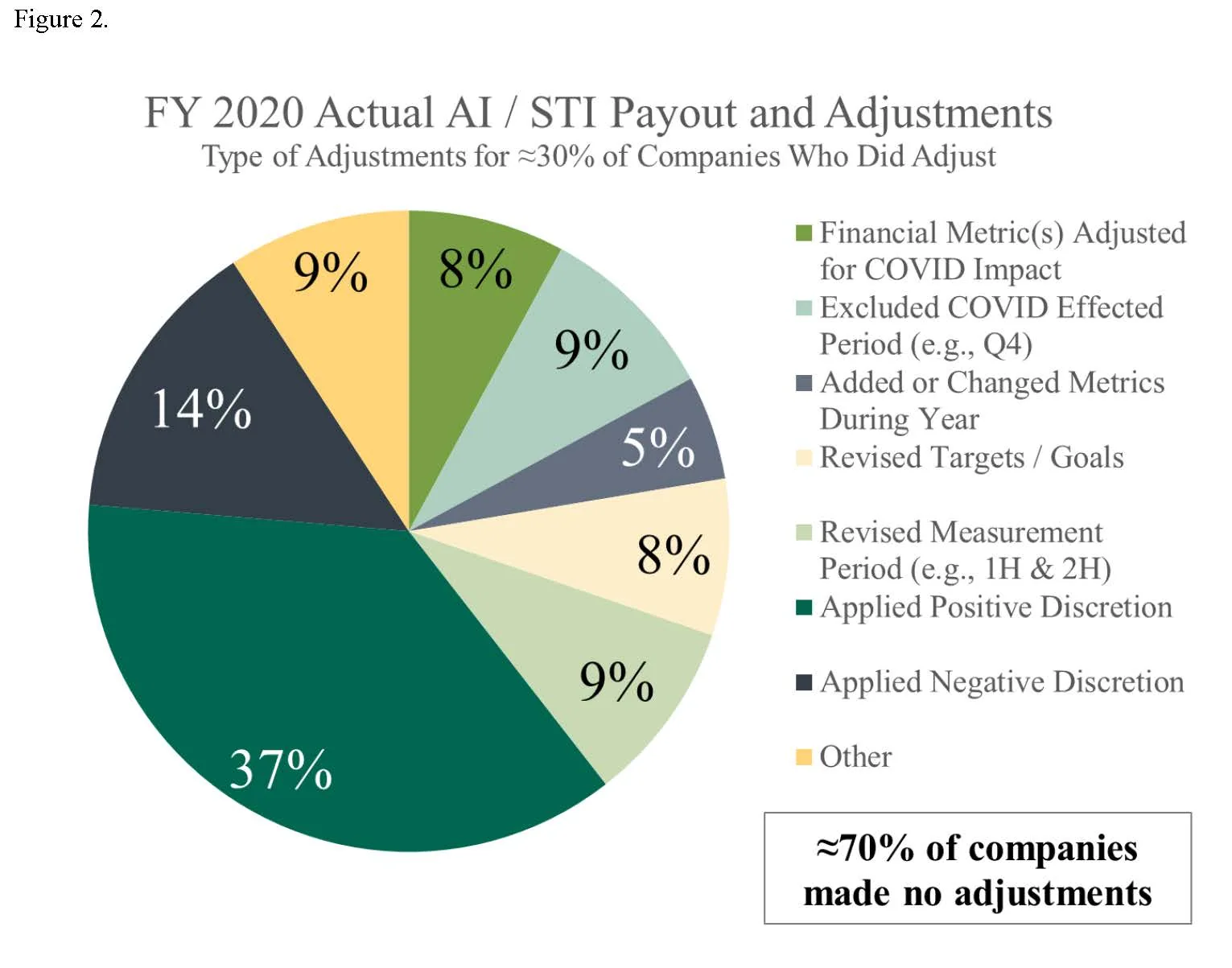

As shown in Figure 2 on the next page, most companies that adjusted AI payouts for the impact of COVID-19 relied on compensation committee discretion ” either positive or negative. Other actions included:

- Excluding financial results for a portion of the performance period (e.g., April-June) affected by COVID-19;

- Adopting revised measurement periods and calculating performance for each period separately;

- Approving a plan adjustment to exclude the impact of COVID-19; and

- Relying on non-financial metrics (predetermined or those adopted in response to COVID-19).

It is important to note that companies with individual performance metrics appear to have incorporated modified performance criteria (beyond what was established at the beginning of the year) to include COVID-19-related actions.

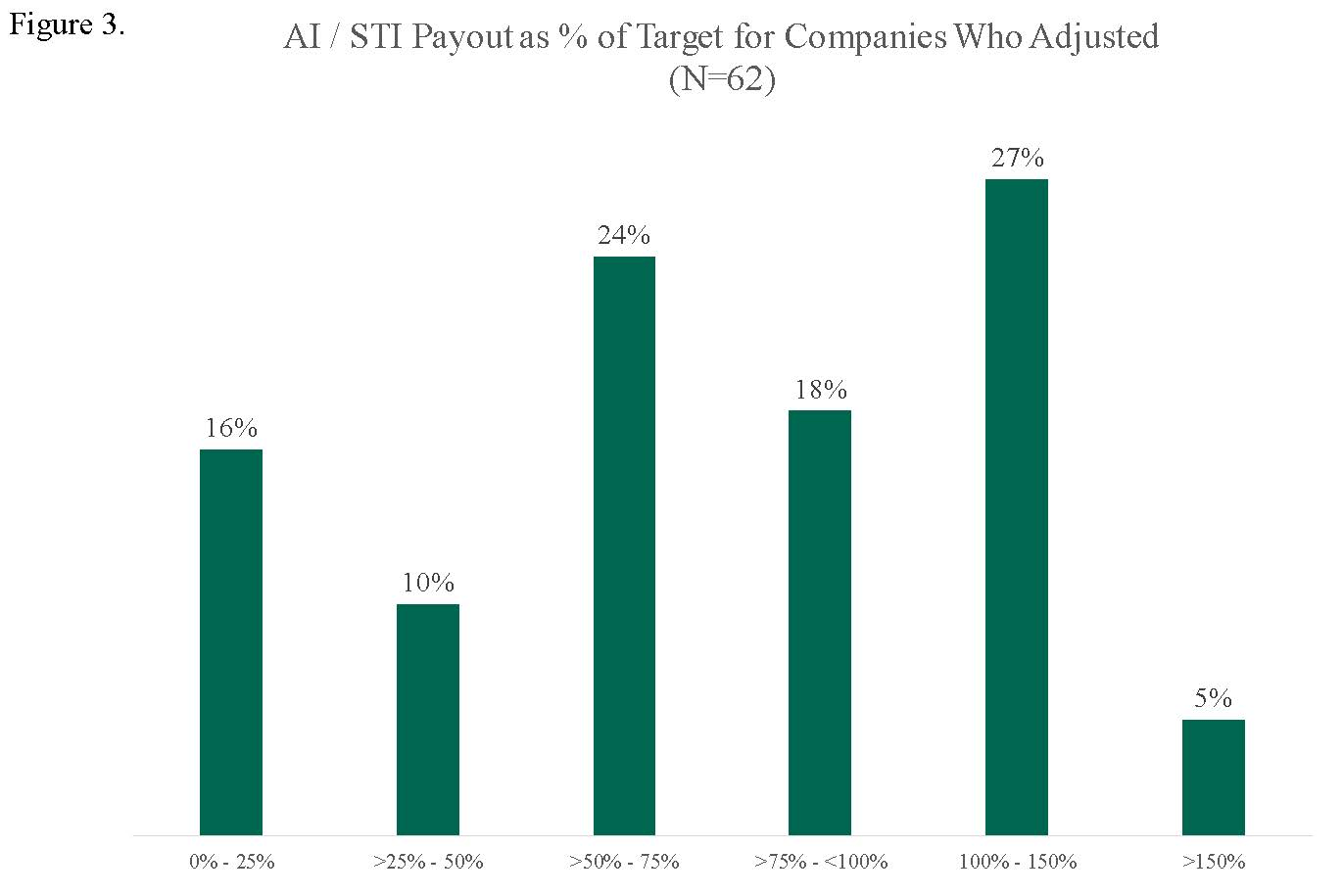

As shown in Figure 3 below, the vast majority of companies that adjusted AI plan payouts kept the final payout below target.

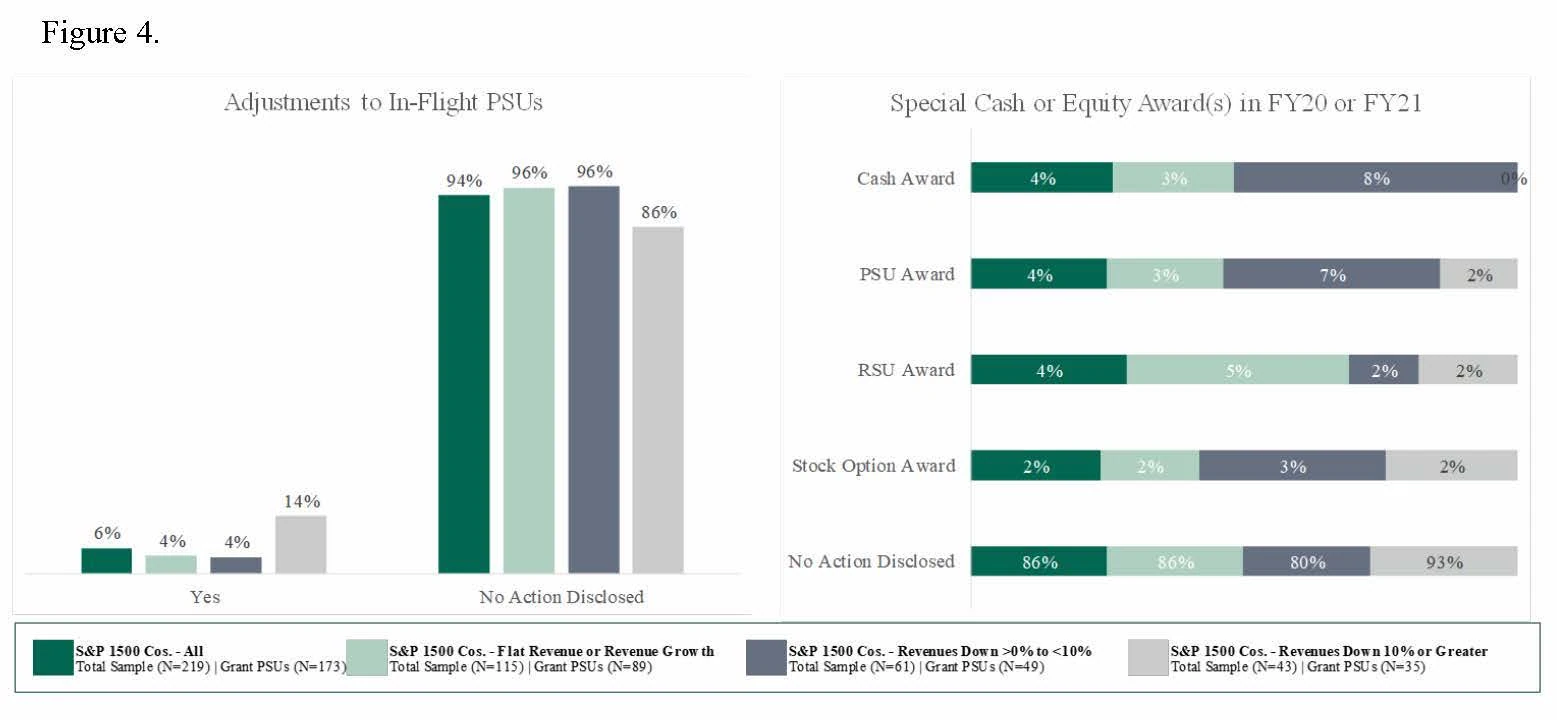

As shown in Figure 4 on the following page, most companies did not adjust their in-flight PSU plans (i.e., those with ‚â•1 year remaining in the performance measurement period) due to:

- Limited visibility into future performance expectations;

- Likelihood of heightened scrutiny by proxy advisors and investors; and

- Disclosure of the increased value of modified awards in the Summary Compensation Table and Grant of Plan Based Awards Table under the accounting modification rules and the added accounting expense.

Also shown below, special, one-time awards (cash and/or equity) have been observed, but prevalence remains low:

- A limited number of companies made special cash or equity awards in 2020/2021 specifically in response to COVID-19; and

- ISS and Glass Lewis have scrutinized companies making such awards and have generally had an unfavorable reaction regardless of the rationale.

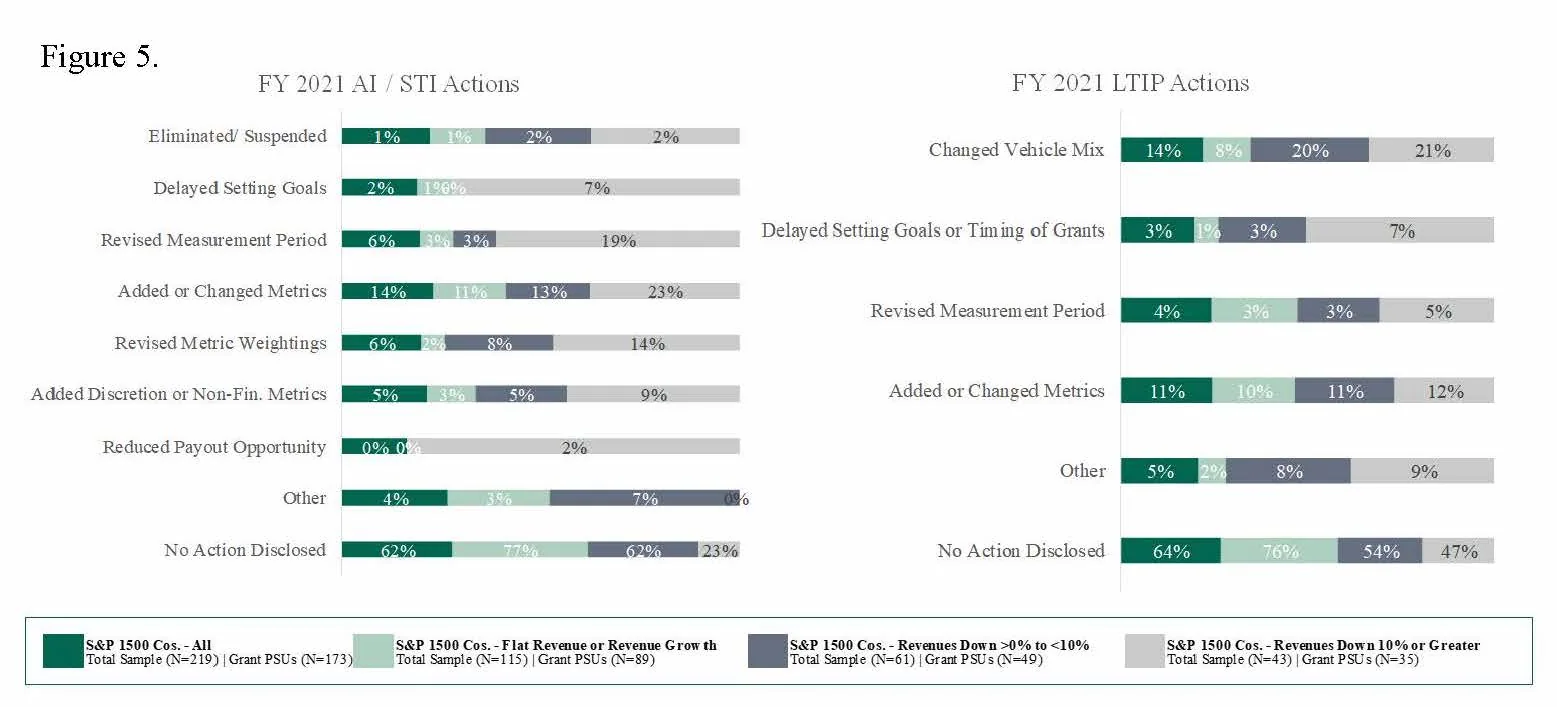

As shown in Figure 5 below, prospective changes to 2021 AI/STI and LTI plans (when disclosed) have been primarily related to metrics and weightings (and, for some AI plans, revised measurement periods).

Considerations

Based on our experience, many companies facing continued uncertainty are considering (or have implemented) an assortment of changes to 2021 incentive designs: setting wider performance goal ranges, adopting an AI plan based on a bifurcated performance period (i.e., first half/second half), adding a non-financial component to the AI plan, incorporating relative metrics in PSUs, and using three 1-year performance goals to measure PSU performance. We anticipate many of these changes are temporary in nature and expect companies to revert to “normal” incentive designs in 2022.

We also believe that 2021 LTI target award values are likely to modestly increase over 2020 levels as companies in severely impacted industries may consider allowing participants to “earn-back” some of the lost value from AI plans and outstanding long-term performance cycles impacted by COVID-19. We also anticipate that lesser-impacted/stronger-performing companies are likely to reward performance and help retain their key talent due to the robust labor market in their respective industries. We advise caution in increasing LTI award values: a significant increase may be difficult to justify when revenue, earnings, and/or stock prices are down or the increase is of such significance it could be viewed as the equivalent of a special LTI award.

Finally, it is to be expected that, as disclosure for companies with calendar year through March 31st fiscal year-end becomes available (i.e., those that have a greater portion of FY 2020 impacted by the pandemic), we may observe increased prevalence of actions taken related to 2020 and 2021 compensation programs.