S&P 500 CEO Compensation Trends – 2024

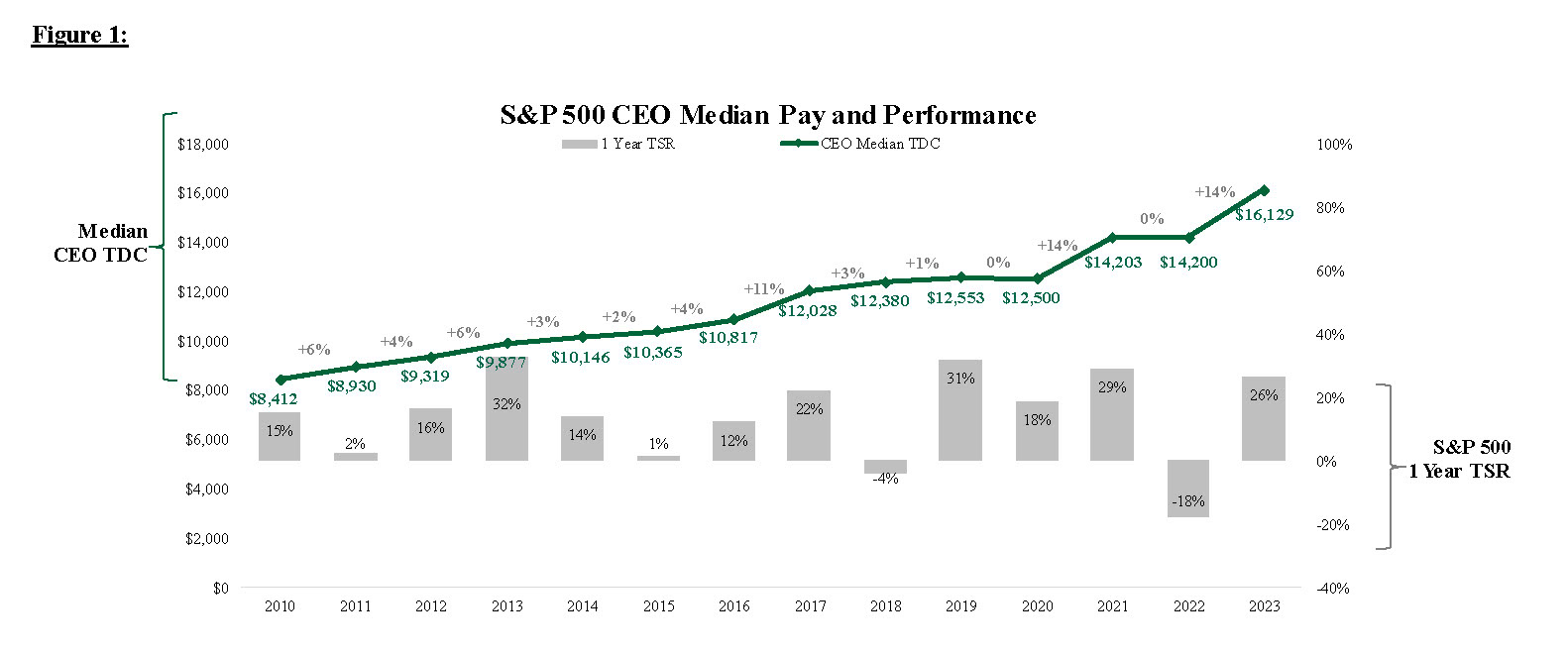

- In 2023, median CEO actual total direct compensation (TDC)* among S&P 500 companies was $16.1M, reflecting an increase of 14% from prior year, driven by an uptick in long-term incentive (LTI) levels.

- The substantial rise in CEO TDC is aligned with a notable 26% increase in 2023 total shareholder return (TSR).

- CEO pay increases are typically correlated with strong TSR performance. In the years TSR was negative (2 of the previous 13 years), CEO pay remained relatively flat. However, in 11 years with positive TSR, CEO pay increased 6%, on average.

- 2024 CEO pay levels will likely increase due to strong TSR of 25%. However, following the high CEO pay increases in 2023, the increase in actual 2024 CEO pay may be more modest. In 2025, following 2 years of strong TSR, we expect CEO target TDC increases will continue though the increases will likely be more modest.

*TDC = sum of base salary, annual actual bonus incentive payments, and the grant date fair value of LTI awards.

Introduction

Following a year of flat S&P 500 median CEO pay from 2021 to 2022, there was a significant increase in median CEO pay in 2023 to $16.1M, reflecting a 14% increase year over year. This shift is correlated with the strong recovery of TSR, increasing 26% in 2023. Our analysis focuses on actual TDC for S&P 500 CEOs with ≥3 years in tenure. Actual TDC reflects the sum of actual salary, bonus incentives (based on actual performance), and reported grant date fair value of LTI awards, including any one-time LTI awards.

Historical Trends in CEO Actual TDC Pay

Historically, CEO actual TDC exhibited modest growth, ranging between 2% and 6% from 2012 to 2016. This trend accelerated in 2017 with an 11% increase, likely driven by sustained robust financial results and TSR performance, before stabilizing to 3% in 2018 and 1% in 2019, aligning more closely with historical norms. Despite strong TSR in 2020, CEO pay remained flat due to the adverse effects of the COVID-19 pandemic. In 2021, CEO TDC reached record highs with a 14% increase, buoyed by exceptional TSR performance. In 2022, both TSR and financial performance decelerated, leading to lower actual bonus incentive payout. Breaking the 2022 plateau, CEO reached an all-time high, driven in part by a robust 1-year TSR of +26%, reflecting one of the highest in 13 years (Figure 1).

CEO Pay Record in 2023 As A Result of Strong TSR Performance

Overall, median CEO pay increased 14% in 2023 driven primarily by an increase in LTI levels (13%) but also by increases across all cash compensation elements year over year: base salary (3%), actual bonus incentives (5%), and CEO TDC increased for most S&P business sectors, with Communication Services and Consumer Staples seeing the highest increases year over year of 23% and 18%, respectively.

As a result of continued strong 2024 TSR performance (25%), we estimate that 2024 CEO TDC levels will continue to rise, driven by actual bonus incentives paying above target levels (with variations by industry) and a likely increase in LTI awards.

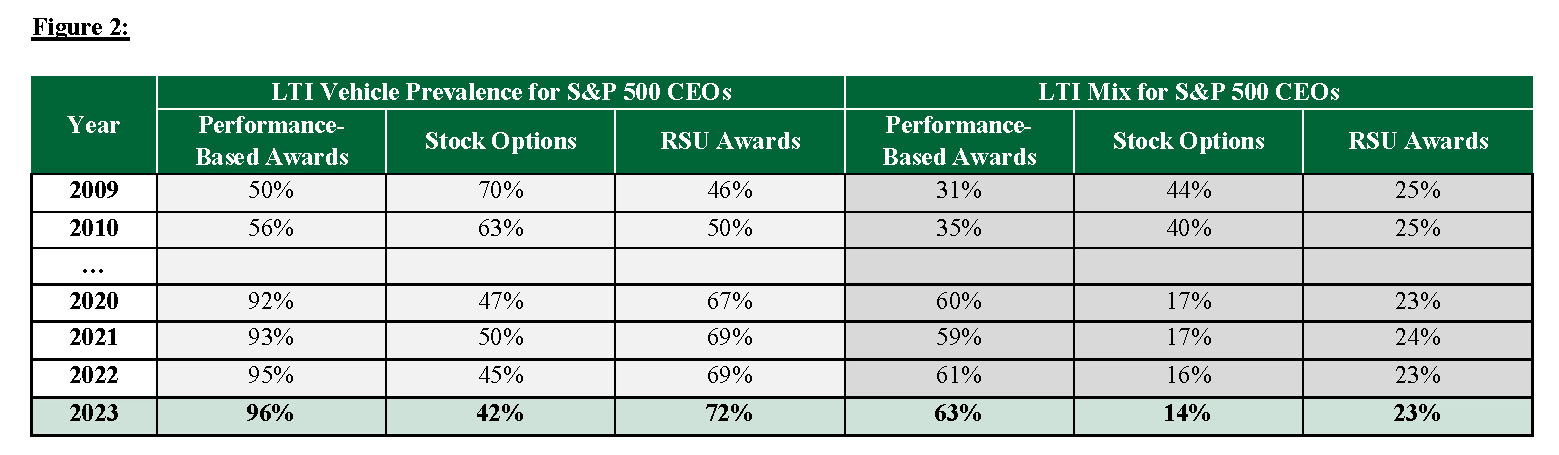

Trends in CEO LTI Vehicles

In 2023, performance-based awards remained the most common LTI vehicle (Figure 2). We observed a slight uptick in the prevalence of time-based awards, with the gap between restricted stock unit (RSU) awards and stock options continuing to widen. The LTI mix trend has flipped from the 2009 mix, where stock options were the most prevalent LTI vehicle.

For 2024 and 2025, we expect the continued dominance of performance-based shares. We note proxy advisor preferences for performance-based awards comprising ≥50% of LTI. Additionally, we anticipate a consistent or slight uptick in LTI weighting of time-based RSUs given their retentive value and as proxy advisors might take a more favorable view of longer-term vesting time-based RSUs.

Trends in CEO Actual TDC versus S&P 500 Index TSR Performance

CEO actual TDC has generally been correlated with TSR performance. In years that TSR was negative (2 of 13 years), CEO pay was relatively flat on average. Conversely, when TSR was positive, CEO pay increased (6%) on average. Although TSR was positive during 2021, due to COVID pandemic, CEO pay remained flat.

In strong stock price environments, compensation committees tend to support CEO pay increases. Annual actual bonus incentive payments, though smaller values than LTI awards, generally pay above target levels (118% bonus payout in FY2023 at median). When companies exceed budget goals as well as investor and analyst expectations, actual bonus incentives often surpass targets, aligning with share price increases driven by strong company performance.

Looking Ahead

Pay Governance anticipates that overall market pay may increase based on solid TSR performance, low unemployment, and favorable macroeconomic trends, including moderating inflation and loosening monetary policy. However, we also expect continued negative pressure on executive pay due to scrutiny from media, government, social activists, proxy advisors, and institutional investors. Below are our CEO TDC projections:

- In 2024, CEO actual TDC is likely to rise due to strong TSR performance. However, given the record-high pay level increases in 2023, the increase in 2024 CEO TDC may be more modest.

- In 2025, following 2 years of strong TSR, CEO target TDC increases will continue, though they will likely be more moderate.

Methodology

The analysis consists of S&P 500 companies led by CEOs with a tenure of ‚â•3 years, designed to highlight true changes in CEO compensation (as opposed to changes driven by new hires or internal promotions, which typically involve ramped-up pay over a period of 1-3 years). Actual TDC reflects the sum of earned salary, bonus incentives (based on actual performance), and reported grant date fair value of LTI awards, including any one-time LTI awards. TDC excludes all other compensation, change in pension values / non-qualified deferred compensation. This differs from target TDC (which represents the target levels for bonuses and LTI, typically set at the beginning of the year) and realizable TDC (which includes in-the money value of stock options, ending period value of time-based awards and estimated value of performance-based awards).