The SEC’s Mandated CEO Pay Ratio in the Context of Income Inequality: Perspectives for Compensation Committees

Key Takeaways

- While the income inequality controversy started as a sociological and public policy debate, Compensation Committees should have a strong understanding of the relationship between public company executive compensation and income inequality.

- The impending disclosure of the ratio of CEO to median employee pay in 2018 proxy statements, as required under Dodd-Frank, will dramatically bring such discussions into the Compensation Committee in the near future. Supporters of the CEO pay ratio believe that this disclosure will reduce “excessive” CEO pay and lower the pay multiple.

- Many blame “overpaid’ executives subject to weak boards and poor corporate governance for being the primary cause of US income inequality. This is not accurate. While corporate executives are paid well, public company executives represent a smaller portion of the highest .1% in more recent times than they did in the mid-1990s.

- Additionally, for the top .1%, growth in public company executive compensation actually lags the growth in private company executive pay and finance professional pay over the same 13-year time period.

- Pay Governance’s analyses of realizable pay for performance indicate that pay-for-performance is operating among US companies.

- Improvements in corporate governance practices combined with similar executive pay levels and designs for private company executives suggest that high levels of public company CEO pay are not the result of corporate governance failure.

- Further, widespread investor support for say-on-pay votes in the past six years indicate broad investor support of the current executive compensation regime.

- We make strong arguments that the CEO pay ratio for a particular company will be indicative of market-driven industry, size and performance factors rather than a failure of corporate governance.

- As Compensation Committees consider the context of inequality issues and executive compensation decisions, Committees should focus on robust corporate governance practices, independent advice, and the company’s strategy for addressing the disclosure of the ratio of CEO to median employee pay in 2018.

Introduction

At a recent Compensation Committee meeting, a director remarked, “As we discuss our CEO’s target compensation for next year, we need to remember that there is an ongoing debate about income inequality.” Income inequality and executive compensation are two of the most controversial issues in modern American economic and political discourse. The forthcoming mandated disclosure of the CEO pay ratio will link these two issues directly in the boardroom.

Many critics blame the rise in inequality over the past 20 years partially or heavily on the rise in public company CEO compensation. These critics use the “300 to 1” large company CEO pay multiple compared to average US employee pay as both the primary symptom and the definition of inequality.1 Inequality is more precisely and typically defined in economics as the percentage of total national income earned by the top percentages of households or taxpayers (e.g., top 1% or top .1%). Using this definition, it is well-documented that US income inequality, historically among the highest relative to other developed countries, has continued to increase significantly. CEO pay also rose over that period.

CEO pay at the largest companies in the US over the past 30 years has grown much faster than average wages”approximately 10.8% versus 4.2% in nominal dollars.2, 3 This is the mechanical explanation for the current differential between CEO and average worker pay”the well-known 300:1 ratio. However, growth in this differential was not an “overnight event.” The rising ratio was the result of very different long-term labor market factors4 which yielded consistent high single digit or low double digit pay increases for top managers over several decades combined with lower wage growth for workers with less valued skills in the market. But is this economic reality the result of failed corporate governance? We explicitly explore this issue below.

How much of the increase in inequality has been caused by CEO pay, and is this a failure of corporate governance? This Viewpoint will provide some insights for directors and others into the answers to these questions in the context of the SEC’s mandated disclosure of the ratio of CEO to median employee pay.

Background

Informed commentary on inequality, including the Conference Board’s recent paper, “Tackling Economic Inequality, Boosting Opportunity: A Blueprint for Business,”5 cites globalization and technological advancement (e.g., office and manufacturing automation) as two driving forces of the recent increase in income inequality in the US. While both phenomena have made material goods more affordable for US consumers, they have also resulted in wage growth that lags the growth in productivity for those workers not participating in high-skill, technology-oriented labor markets or global commerce.

Many commentators cite “excessive” executive pay as one of the primary causes of income inequality.6 Such “excessive” executive pay, they argue, has been created or at least enabled by low/declining marginal tax rates in concert with poor corporate governance practices (e.g., cronyism between the board and the CEO).7 For valid reasons, directors may be inclined to focus on the governance of their own company’s executive compensation programs and ignore the public debate on inequality, some of which is flawed. However, the public discourse can and does enter the board room when directors must consider the media implications of executive compensation decisions.

Most importantly and directly, the SEC’s mandate that public companies disclose the ratio of CEO pay to median employee pay in 2018 proxies will bring the discussion of income inequality further into the Compensation Committee. Supporters of the pay ratio believe that this disclosure will reduce excessive CEO pay at many companies, allegedly caused by weak governance.8 Their theory is that this reduction will lower the 300:1 large company pay multiple thereby reducing inequality; this theory was the genesis of the Dodd-Frank CEO pay ratio.9 Further, income inequality and the ratio of CEO pay to average US worker wage have been cited in at least one shareholder proposal requesting supplemental reporting on the CEO to employee pay ratio and an explanation from the company regarding whether broad-based layoffs or pay cuts warrant changes to executive pay.

Therefore, it is critical that Compensation Committee members maintain a perspective and philosophy from which to govern executive compensation in a world where income inequality is a major public policy issue. This viewpoint addresses several key questions and criticisms regarding the economics, corporate governance and structure of executive compensation as they relate to the broader issue of income inequality.

Question 1: Is the recent increase in US income inequality caused primarily by the increase in the number of public company executives in the top .1% of earners?

No, not primarily. Clearly, corporate executives have among the highest paying jobs in the US economy (along with lawyers, finance professionals, entertainers and athletes), and growth in executive pay levels of corporate executives at publicly-traded companies explains some of the increase in income inequality in the US. Nevertheless, a definitive study on the occupations of high income taxpayers demonstrates that the compensation of public company executives is not the primary cause of the increase in inequality.

Corporate executives are a shrinking minority of .1% income earners

Many critics argue that the large increase in executive pay has been a major cause of the increase in income inequality. Thomas Piketty, the author of the recent seminal and controversial book on income inequality states, “The final and perhaps most important point in need of clarification is that the increase in very high incomes and very high salaries primarily reflects the advent of ‚Äòsupermanagers,’ that is, top executives of large firms who have managed to obtain extremely high, historically unprecedented compensation packages for their labor.”10

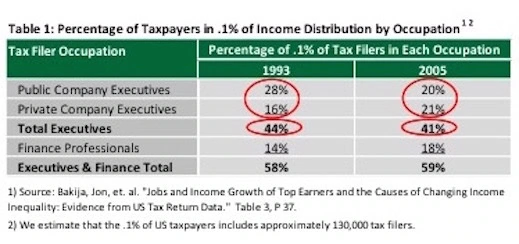

A prominent study by economist Jon Bakija on the individuals composing the top 1% and .1% of the income distribution by occupation up until 2005 provides valuable insight into the role that corporate executive pay plays in the .1% of total incomes.11 The study finds that public company executives comprise an important minority”20% in 2005″of the share of the top .1%. However, the relative share of public company executives in the top .1% declined substantially over the prior decade”from 28% in 1993 (see Table 1 below). This decline in the share of public company executives in the .1% of the taxable income distribution occurred concurrently with the share of private company executives and finance professionals increasing as a portion of the .1% over the same time period (to 21% and 18%, respectively, in 2005). Many critics erroneously conflate the increase in income for private company executives and finance professionals with public company executives. The growth of the size of the financial sector is a valid public policy question, but it is an issue that is beyond the ken of this paper and should not be part of the corporate governance debate that resulted in the CEO pay ratio mandate.12

Question 2: Alternatively, is the recent increase in US income inequality caused primarily by the increase in the aggregate pay levels of public company executives in the top 1% and .1% of earners?

No. The data in Table 1 shows that it is not the increase in the relative number of executives in the top .1% that is the primary cause of the increase in income inequality for the top .1%. Next we explore whether the increases in the aggregate pay levels of the highest paid public company executives is a primary cause of the increase in income inequality.

Public company executives’ pay growth below private company executives’ growth

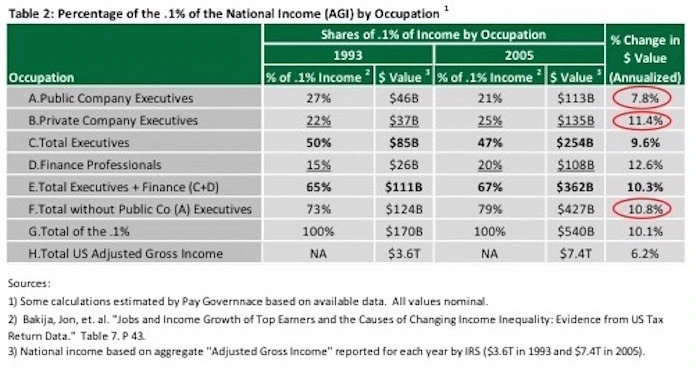

The same data set from Bakija referenced above shows the trends of the incomes for the various professional groups representing the .1% of income earners”see Table 2. Specifically, the 7.8% twelve year [1993-2005] annualized increase in aggregate taxable income for the public company executives, while higher than the 6.2% growth in total gross income, was much lower than the 11.4% annualized increase in incomes for private company executives, the 12.6% increase for finance professionals, and the 10.8% increase for all of the .1% income bracket excluding public company executives.

Some critics doubt the competitiveness of the corporate executive labor market based simply on absolute aggregate compensation levels or the historical increase in pay for public company executives. However, the fact that public company executive income growth lags the income growth of other groups in the .1% income distribution suggests that the growth in public company executive pay, and the governance context in which it is set, is not out of line with other high income earners.13

Question 3: Is CEO pay aligned with the performance of their employer?

Yes. An important consideration in the inequality/CEO pay debate is whether the pay of executives is aligned with the performance of the company that he or she manages. This is arguably the key factor that is under the control of the Compensation Committee. The objective reality is that the vast majority of companies are doing an excellent job of ensuring such alignment.

Our firm’s compensation consulting experience and research show that executive pay is highly aligned with company performance. Further, market data on public company pay philosophies indicate that most public companies today target executive pay opportunity at the median of a peer group of similarly-sized companies and rely almost exclusively on actual company performance to determine the amount of pay ultimately realized or realizable. Pay Governance has conducted many 3-year studies of CEO realizable pay-for-performance for numerous industries and for all S&P 500 CEOs, plus a 10-year period study. All of these studies confirm that strong pay-for-performance alignment is operating among US public companies.14

Question 4: Have corporate governance failures caused excessive executive compensation levels at public companies, thus exacerbating the inequality issue?

Generally, no. Many critics, when pressed for a mechanism by which corporate executive compensation is set inappropriately, cite flawed corporate governance as the driving force behind executive compensation growth. These criticisms have two aspects: too much focus on creating shareholder value [rather than adding other stakeholders]15 and specific policy flaws in the governance process that weaken board oversight on executive pay. We present several perspectives on the US corporate governance climate that refute these claims. In fact, governance has improved substantially over the past 20 years, the same period during which executive pay increased. Further, shareholders appear highly satisfied with the US executive pay model which is heavily linked to the creation of shareholder value.

Has US Corporate Governance Improved Substantially over the Past 20 Years

Yes. Using numerous standardized and researched metrics, US corporate governance has improved and public companies have addressed many prior criticisms.16 These improvements in governance best practices17 include: a significant increase in shareholder outreach; an increase in the percentage of independent directors; annual elections for directors; more separate chairs and near universal prevalence of lead directors; independent board nominating committees; elimination of “poison pills”; enhanced proxy disclosure and proxy access; among others.18 Specifically, in executive compensation governance, there have also been many changes/improvements responding to shareholders, proxy advisors and political pressures: say on pay votes; elimination of single trigger stock acceleration and excise tax gross-ups at a change in control19; reduced pensions; introduction of anti-hedging and anti-pledging policies; increases in performance vesting for stock grants; introduction of clawbacks; etc. While some of these are disputed as true enhancements, taken in total, US corporate governance has improved significantly while executive pay has increased.20 These improvements are a direct rebuttal to the “weak governance of CEO pay” explanation of inequality.

Private Companies With Direct Owner Representation Have Similar Executive Pay Growth

Some critics argue that poor governance by public company Boards and Compensation Committees has caused the excessive growth in public company executive compensation. However, as illustrated in Table 2, the 11.4% income growth for private company executives in aggregate (relative to 7.8% for public company executives) refutes the arguments criticizing public company governance. Private company executive compensation is set either by individual private company shareholders or a Committee of private equity managers who hold a direct stake in the financial success of the companies. Said another way, there is no separation between the shareholders (principals) and the Committee setting pay for the executives. Even in this supposedly superior governance environment, income for highly-paid private company executives, in aggregate, grew faster than those for public company executives. This suggests that private equity owners, just like public company shareholders and the Boards that represent them, believe that using large amounts of performance-based equity grants is the best way to align executive management’s personal interests with the financial interests of the owners of the company.

Collectively, these are strong arguments that the CEO pay ratio for a particular company will be indicative of market-driven industry, size and performance factors rather than a failure of corporate governance.

Question 5: Are shareholders dissatisfied with the US executive pay model?

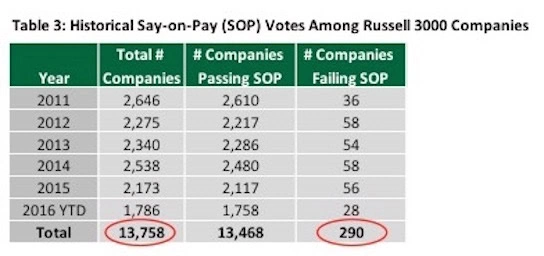

No. Corporate shareholders certainly appear to agree with the current executive compensation structure. As a group they have provided an advisory vote in favor of executive compensation programs at the vast majority of companies. Specifically, there have been only 290 failed say-on-pay votes among 13,758 say-on-pay votes for Russel 3000 companies – a failure rate of just 2.1% – over the past six years.22 This is a stunning statistical indicator of shareholder support. Even ISS, the influential proxy advisor to institutional investors, recommends a “for” vote for nearly 90% of companies. These statistics indicate that the shareholders are highly supportive of the current pay-for-performance model for US public companies overall. This support appears to include the broad emphasis on incentives for shareholder value creation that most US companies utilize. CEO pay ratios need to be viewed in the context of this broad shareholder support.

Considerations for Compensation Committees in Evaluating their CEO Pay Ratio

The conclusion of our research is that relatively high executive compensation at public companies, allegedly enabled by compliant boards, is not the primary explanation for rising income inequality in the US.

Compensation Committees must continue to govern executive compensation levels and designs to motivate the executive team to maximize shareholder value in the context of the broader public debate on income inequality and executive compensation. Committees cannot and should not directly address the criticism regarding the “300 to 1” large company CEO pay multiple compared to average US employee pay. However, Committees should maintain focus on best practice executive compensation governance, and consider whether additional information or analysis on internal pay equity may be helpful, as they evaluate their own CEO pay ratio:

1) Ensure that competitive executive compensation opportunity levels are monitored annually against the median of an appropriately-sized peer group. This will provide a robust context for the CEO pay ratio.

2) Ensure that executive compensation program design provides appropriate pay-for-performance linkage, including setting challenging performance goals and providing the majority of compensation in long-term equity.

3) Apply best-practice compensation policies including robust stock ownership guidelines, clawback provisions, and prohibitions on hedging and pledging company shares to further link executive income and wealth to the performance of the company.

4) Maintain strong corporate governance practices including nominating directors using an independent Nominating Committee, using independent compensation consultants and legal counsel, and holding executive sessions at each Compensation Committee meeting.

5) Ensure that all employees are competitively and appropriately paid relative to the profitability, fairness and economics of the company.

6) Consider whether the Compensation Committee should review supplemental analyses related to the CEO pay ratio and broad-based pay practices (e.g., comparison of executive versus broad-based pay increases, review of number of employees covered under benefit programs, and review of pay ratio and median employee data to peers).

7) Consider how the Company will address and explain the disclosure of the ratio of CEO to median employee pay in the 2018 proxy. Since supporters of the CEO pay ratio believe that this disclosure will reduce “excessive” CEO pay caused by weak governance, companies may need to be explicit in responding to this theory. The data and analysis presented here could help in this regard.

____________________________________