Are Institutional Investor Preferences for Performance-Based Equity Really Diminishing in Favor of Time-Based Shares?

Introduction

Recent statements and opinions made by proxy advisors, a Europe-based institutional investor, and some academics and consultants have cast the preference for using performance-based equity incentives into question. The use of these plans, such as performance share units (PSUs), has become nearly universal and is the largest form of compensation delivered to S&P 500 chief executive officers (CEOs). This practice has largely been due to previous proxy advisor requirements, and investor preferences, that PSUs or other performance-vesting equity comprise at least a majority of CEO total equity compensation.

As demonstrated in this Viewpoint, our investor opinion survey conducted this summer shows that the vast majority of shareholders strongly prefer that companies continue the majority usage of PSUs, and it does not indicate much preference for movement to long time-vesting restricted stock units (RSUs). Our survey conducted in partnership with IR Impact of more than 100 large investors revealed:

- 71% of investors prefer that issuers (publicly-traded companies) continue using PSUs, often in combination with a balance of time-based RSUs, and

- 86% desire that PSUs comprise at least 50% of total long-term incentive (LTI) value awarded to executives.

Critiques of PSUs

The recent criticisms of the use of PSUs have largely focused on three themes:

- PSU plans are too complex: “Current structure of long-term incentives is unnecessarily complex” and “multiple forms of incentives and performance metrics have contributed to the rise in executive pay.”[1]

- PSUs are misaligned with shareholder investment returns, and companies granting PSUs provide higher compensation for lower performance than those companies that use time-based equity vehicles.[2]

- Use of relative total shareholder return (rTSR) is not an effective motivational incentive metric despite its direct alignment to the shareholder investment experience.

In response to some of these criticisms, both Institutional Shareholder Services (ISS) and Glass Lewis have included topics in their annual policy surveys asking survey participants for their opinions on the use of performance-based and time-based equity plans, including the relative emphasis preferred on both vehicles. To date, the proxy advisors appear to be mixed/ambiguous on this important topic.

The ISS 2024 policy survey indicated that a minority (31%) of investors thought ISS should revise its current approach and begin considering the use of time-based equity awards with extended vesting periods to be a positive mitigating factor when there is a pay-for-performance misalignment. A larger group of investors (43%) responded that a predominance of time-based equity awards should continue to be viewed as a negative factor in the context of the presence of pay-for-performance misalignment.[3] In contrast to these results, ISS has also stated “many investors are calling into question the presumption that performance-conditioned pay is preferable to other forms of executive pay.”[4]

The Glass Lewis 2024 policy survey more directly asked investors about their preference of LTI vehicles. Only 15% of investors agreed that they “prefer time-based equity awards over performance-based equity because the vesting conditions for performance-based equity have become too complicated and difficult to monitor.” As further evidence of investor support for PSUs, the Glass Lewis survey results indicated that 92% of investors agreed “a large portion of equity compensation should be performance-based to ensure that executive pay is aligned with performance results.”[5]

Likely influenced by the proxy advisor pay-for-performance models, 93% of S&P 500 companies use PSUs; these plans on average make up about one-third of CEO target total compensation.[6] There clearly was and has been strong shareholder support for the CEO pay model as evidenced by high average Say on Pay votes (2011-2024 average S&P 500 “for” vote of 90% and 98+% of votes passing).[7]

Recent regulations to require the Compensation Actually Paid (CAP) disclosure in the proxy also helped support the notion that CEO pay has been aligned with performance. Pay Governance research on PSU plan payouts and TSR performance confirmed that PSU payouts are aligned with shareholder outcomes. This may partially explain why shareholders have consistently and strongly supported Say on Pay since its inception. As further support against the above criticisms of PSUs, Pay Governance and a few others extensively studied the PVP/CAP 2022 regulation and found it to demonstrate very strong pay and performance alignment. If CAP is high or growing, it will be aligned with TSR and the obverse will also be true (low/decreasing CAP aligned with low TSR).[8]-[10]

Specific Findings from our Large Investor Opinion Survey

Pay Governance in collaboration with IR Impact, a leading governance and investor relations intelligence firm, surveyed more than 100 institutional investors and public pension funds with aggregate assets under management (AUM) of $29 trillion. Our objective was to understand investor perspectives on the use, design, and disclosure of PSUs given recent media coverage of this important and prevalent compensation component. While the design and mix of LTI awards need to be driven by each company’s unique cultural and strategic situation, understanding investor preferences is also critical.

Our survey sample included institutions with an average AUM of $261 billion and included responses from portfolio managers, investment analysts, and governance/stewardship officers. The participants were based across North America (59%), Europe (40%), and Asia (1%).

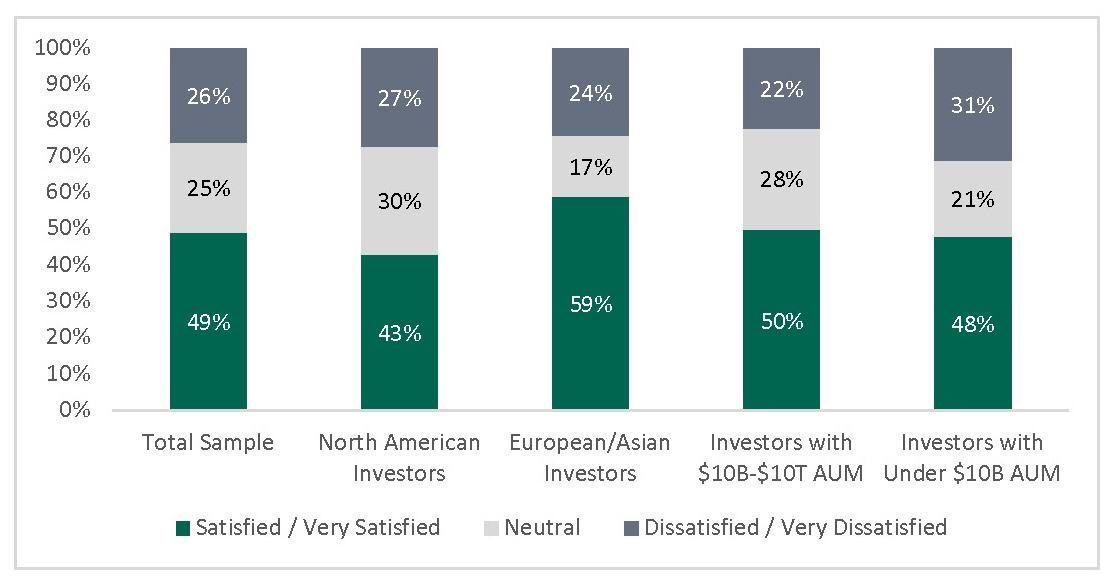

In general, our survey respondents expressed satisfaction that executive pay is aligned with shareholder performance, much of which is explained by the large amounts of PSUs granted (see Exhibit 1). Nearly one-half (49%) of all investors indicated they were satisfied / very satisfied with the CEO pay alignment at their portfolio companies while only about one-quarter (26%) were dissatisfied or very dissatisfied. Investor sentiment was similar across regions and AUM.

Exhibit 1: Investor Sentiment Toward Executive Pay and Performance Alignment

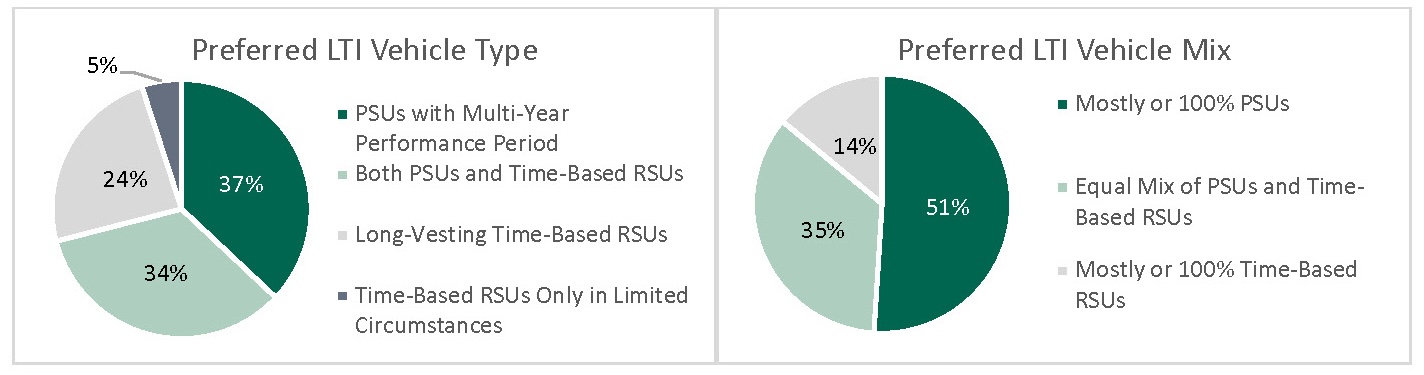

As shown in Exhibit 2, the results of our survey largely support the preference for PSUs in contrast to time-based stock awards (RSUs) with longer vesting schedules than typical: 71% preferred PSUs that would be earned/vested over a multi-year period or PSUs in concert with a balance of time-based RSUs. A majority (51%) would rather have issuers award mostly or 100% PSUs, while a sizeable group (86%) desire that PSUs comprise at least 50% of total LTI value. Importantly, from most executives’ point of view, the upside payout of the number of PSUs (150-200% of target) is extremely compelling and motivational relative to RSUs that do not have that type of upside. Investor opinions are split on whether standard stock options with time-vesting are considered performance-based (52%) or time-based (48%).

Exhibit 2: Investor Preferences of LTI Vehicles

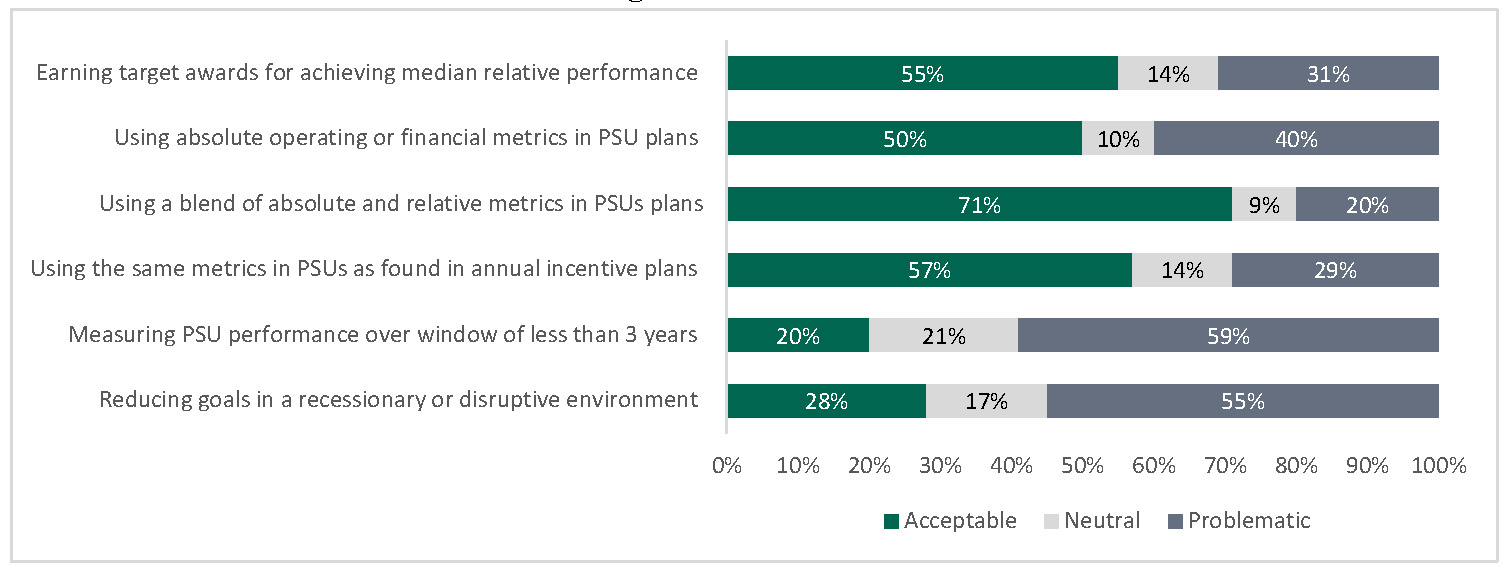

From a design and disclosure perspective, investor preferences from our survey generally mirror current typical practices (see Exhibit 3). Such practices include paying out at target for median (50th percentile) relative performance, using a blend of absolute and relative metrics (some of which may overlap with annual incentive metrics), and measuring PSU performance over a multi-year period of at least 3 years. In terms of PSU metrics, most (91%) investors prefer financial metric(s) linked to the issuer’s disclosed strategy or a mix of financial metrics and stock-price metrics (absolute or relative). The majority (55%) of respondents indicated it would be problematic to lower performance goals year-over-year in recessionary or disruptive environments. Lastly, and in contrast to common practices, most investors (84%) agree that issuers should forward-disclose PSU multi-year financial performance goals in their CD&As. Based on information collected from ESGAUGE, we found that of the S&P 500 companies that use 3-year financial metrics, 40% forward-disclosed their goals in 2025 proxy statements.

Exhibit 3: Investor Preferences of LTI Design and Disclosure Practices

Shareholder Engagement Disclosure

Pay Governance reviewed the shareholder engagement efforts disclosed by nearly 200 S&P 500 companies in 2024 and 2025 proxy filings and extracted investor feedback related to LTI programs.[11] The most frequently cited areas of investor feedback on LTI programs were around design features of PSU plans (e.g., types of metrics used, length of the performance period, difficulty of the performance goals). The next most common area of investor feedback was around the mix of LTI vehicles and, more specifically, the proportion of LTI denominated in PSUs. When commenting on the use of PSUs, most investors expressed strong support for PSUs to increase the alignment of executive compensation with Company performance and, in some cases, conveyed the preference for the majority of LTI value to be delivered in PSUs.

Conclusion

Anecdotal criticisms of PSUs should be considered thoughtfully and not compel a change in approach. Rather, it is important to have a clear understanding of the preferences of shareholders and to ensure the LTI program supports long-term strategic priorities and aligns with the company’s executive pay and performance philosophy. Most companies can and likely will continue with the vast majority of their executive pay practices, as they have been highly motivational, aligned with stock price performance, very successful, and endorsed by the shareholders.

General questions about this Viewpoint can be directed to Ira Kay (ira.kay@paygovernance.com), Linda Pappas (linda.pappas@paygovernance.com), or Lane Ringlee (lane.ringlee@paygovernance.com).

__________________________