Effectively Administering Your Relative TSR Program – Learning and Best Practices

Key Takeaways

- Relative TSR plans have grown in prevalence and are now used by approximately 50% of companies.

- Companies should understand the implications on share grants and proxy disclosed compensation values associated with using either the accounting fair value or grant date stock price to determine the number of TSR shares to grant participants.

- Relative TSR plan grant agreements should contain specific details regarding:

– The approach for calculating the starting and ending stock price for determining TSR

– The definition of stock price (closing or average high/low)

– How to treat stock splits and dividends in the TSR calculation

– The methodology, either “Ranking” or “Percentile”, used to calculate TSR performance

– How to treat changes to peer companies during the performance period due to a bankruptcy, merger or acquisition, a spin-off or divestiture, or if a peer is delisted from a major exchange

- Given the number of nuances and in order to enhance the governance and credibility of the plan, companies should consider using an external provider to conduct the accounting valuation and calculations of performance on an interim and final payout basis.

Introduction

Relative TSR is a performance metric most often used in LTI performance plans. Its use as a metric has nearly doubled over the past 5 years and is now used by approximately 50% of companies spanning all sizes and industries. While the appeal of this metric for shareholders and directors alike is its alignment with shareholder value creation and the absence of having to establish long-term performance goals, there are other nuances and considerations that can make the administration of these plans much more complex than other types of arrangements. Over the years, our experience in designing and assisting companies with administering relative TSR plans has led to a series of best practices that are the focus of this article. These practices are less about contemporary design issues, and more about ensuring the appropriate provisions and methodologies are in place to enhance the governance of relative TSR plans from the time of grant to the calculation of payouts. They include:

- understanding the implications of award valuation on the number of shares granted;

- understanding the nuances of the TSR definition;

- selecting a method for calculating relative TSR performance;

- recognizing peer group changes that occur during the performance period; and

- enhancing plan governance.

Understanding the Implications of Award Valuation on the Number of Shares Granted

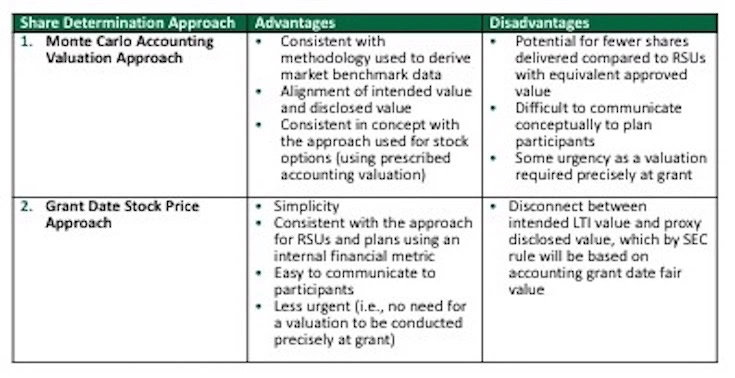

Given the use of a market condition (stock price) to measure performance in relative TSR plans, companies are required to use a Monte Carlo valuation methodology to determine the grant date fair value for accounting and proxy disclosure purposes. This approach is different than the approach used for accounting and disclosure purposes for restricted stock or performance plans based on an internal financial metric. For those types of awards, the fair value represents the stock price on the grant date. The Monte Carlo valuation approach used to value relative TSR plans typically results in a fair value that is 10% to 20% or more higher than the stock price on the date of grant depending on the design. When determining how many relative TSR shares or units to grant a participant, compensation committees typically choose to divide an intended value by either the Monte Carlo accounting fair value per share or the grant date stock price; this is consistent with the approach used to determine share grants for restricted stock or performance awards using an internal financial metric. The following table illustrates the implications of the 2 approaches:

Using the Monte Carlo accounting fair value approach will almost always result in fewer shares at grant given the valuations’ associated premium. However, this approach provides consistency between the intended value to be delivered at grant and that disclosed in the summary compensation table of the proxy statement, which is often desired by compensation committees. However, some companies believe that a performance metric, whether TSR or an internal financial metric, should have no bearing on the number of shares granted. These companies will often use the grant date stock price to determine the number of shares to grant. This approach will create a difference in the intended grant value and the value for accounting and disclosure purposes. In our experience, approximately 60% of companies use the Monte Carlo accounting fair value approach, and 40% use the grant date stock price approach. Neither approach is inherently “right” or “wrong,” but committees should be mindful of the relative advantages and disadvantages of each approach in making their decision when calculating share grants for their relative TSR awards.

Understanding the Nuances of the TSR Definition

Developing a well-written relative TSR plan grant agreement is critical to ensuring strong plan governance. Relative TSR plans have unique design provisions that are easy to overlook; even the most comprehensive grant agreements should be reviewed annually to ensure they appropriately reflect the intentions of the plan. Ultimately, a well-drafted grant agreement mitigates the potential for stressful conversations arising from differing interpretations of plan provisions at the time of payout. Among the many important considerations for an award agreement, we outline a few key areas companies should define clearly:

- Clarify the start and end date measurement period and definition of stock price used to calculate TSR ” The grant agreement should clearly define the performance period (including the start and end date), whether a multi-day average will be employed based on calendar days or trading days, and whether TSR should be calculated using stock price close or an average of high/low. If a multi-day average is used, companies should clearly define the treatment of dividends during the averaging period.

- Treatment of stock splits ” Stock splits may occur among some peer companies during the performance period. The grant agreement needs to provide guidance on the treatment of stock splits. Typically, this guidance provides for the stock price at the beginning of the performance period to be appropriately adjusted to reflect the split. Stock splits usually garner far less attention than an acquisition or bankruptcy. Companies need to be vigilant in looking for stock splits among peer companies over the course of the performance period.

- Treatment of annual and special dividends ” The treatment of dividends is generally defined either by reinvesting the dividends when they are announced/paid or by treating the dividend as a cash payment to be added to the final price. Specifying the dividend treatment is especially important in industries with higher dividend yields (eg, REITs, banks, utilities, etc), which can have a larger impact on relative performance results and payout. Special one-time dividends or other distributions to shareholders (eg, for divested businesses) should be considered when defining dividend treatment. The treatment of annual and special one-time dividends within the TSR calculation should be consistent among the company and its peers.

Methodology for Calculating TSR Performance

The grant agreement should specify whether TSR performance will be calculated using either the “ranking” or “percentile” methodology. With the “ranking” methodology, the payout schedule is dependent on the company’s rank among peers (eg, a rank of fourth among 13 peers results in a predetermined payout). With the “percentile” methodology, the payout schedule is dependent on the company’s TSR versus calculated percentiles of the peers (eg, 30th percentile TSR results in a threshold payment). We believe both methodologies are reasonable; however, the use of the “percentile” methodology would be more accurate for peer groups containing fewer companies.

Changes to the Peer Group during the Performance Period

It will be nearly inevitable that a change will occur to at least one peer company during the performance period, which is typically 3 years in length. These changes typically take the form of a bankruptcy, merger and acquisition activity, a spin-off or divestiture, or a peer company delisted from a major exchange. Grant agreements need to address the treatment of these events in order to provide guidance when they occur. While many companies will include a provision that provides the Compensation Committee with the discretion to handle these events as it deems appropriate, there are a series of best practices that are usually followed:

- Bankruptcy. Most companies view a bankruptcy as an event that falls within management responsibility. Therefore, bankrupt companies are usually moved to the bottom of the peer group under the “ranking” methodology or given a -100% performance under the “percentile” methodology. Under both methodologies, the company remains in the peer group and is counted for performance purposes.

- Merger or Acquisition. In most instances, acquired or merged peer companies are removed from the peer group and TSR calculation. If a peer company acquires another company that significantly alters its business focus, it too would generally be removed. However, the acquisition of small businesses is often a routine event for many companies. In these instances, the peer typically remains in the peer group when calculating TSR. A discretionary provision is helpful in making these judgements.

- Spin-off or Divestiture. These types of transactions have become fairly common. In the event that a spin-off or divestiture materially changes the focus of the business, the company should be removed from the peer group and TSR calculation. However, if the remaining business is viewed as viable, and continues to be in alignment from a business focus, then the grant agreement needs to specify how to treat the conversion of stock and any special cash payment made to shareholders. In these instances, any stock provided in the new company could be assumed as sold as of the conversion date and treated like a dividend.

- Delisted from Major Stock Exchange. In most cases, peer companies who are delisted or traded on pink sheets are treated similarly to a company who enters bankruptcy. In this instance, the company is moved to the bottom of the peer group under the “ranking” methodology or given a -100% performance under the “percentile” methodology.

Enhancements to Plan Governance

Accurately administering a relative TSR plan can be a challenging exercise given the complexities associated with applying the terms of the award. Even the most comprehensive grant agreement often requires interpretation and discretion that can impact award payouts. Given these complexities, we believe companies benefit from having an external advisor assist with the administration of outstanding plans, including the valuation of the grants for accounting and disclosure purposes. Many of the events identified above can meaningfully impact the award payout. To the extent that an event is not clearly addressed in the grant agreement, the external advisor can serve as the arbiter, independently facilitating a discussion of the issue with management and the Compensation Committee as well as providing market context in terms of how other companies might address the situation. The external advisor can also serve to calculate interim and final performance on outstanding plans. The benefits of these activities allow for:

- independent interpretation of the plan provisions to be applied consistently throughout the performance period;

- calculation of interim performance results, which can serve to keep the compensation committee informed (typically on a quarterly basis) and be shared with plan participants as a communication tool to increase the incentive value of the plans and enhance line-of-sight; and

- calculation of final performance results, which can build payout credibility through the accurate and consistent application of plan provisions.

Conclusion

As relative TSR plans have increased in prevalence in recent years, companies have been presented with several challenges that are unique to their design. Arguably, while relative TSR plans alleviate the challenges of having to establish long-term performance goals, the administration of these plans can be more challenging than performance plans based on internal financial goals. Companies would benefit from reviewing their grant agreements to ensure they properly address the definition of TSR, the specific methodology used to calculate performance, and the addressing of changes that may occur to the peer group during the performance period. Proper administration and governance can enhance the credibility of these plans among participants and shareholders.