Selecting Optimal Incentive Measures: The Role of TSR Correlation Analysis

- Selecting appropriate incentive performance measures is a critical responsibility of the Compensation Committee and management.

- It is important to consider several perspectives when identifying or confirming incentive plan performance measures.

- While business strategy should be the primary focus when selecting performance measures, it is insightful to consider how TSR correlates to various performance measures over time.

- These correlations can vary by industry and business model.

Summary

The selection of appropriate performance measures to use in incentive programs is a critical decision for management teams and Compensation Committees. While a company’s business strategy should be the primary factor when selecting incentive plan measures, it is insightful to consider other perspectives, such as historical results and market practices. In this Viewpoint, we discuss the role that total shareholder return (TSR) correlation analysis can play in performance measure selection.

TSR correlation analysis assesses the historical relationship between TSR and measures of financial performance. The TSR-financial performance correlation analysis can be measured using a company’s own history (internal perspective) and a peer set (external perspective). Correlation is not causation. Rather, these analyses assess the degree to which a financial measure moves in the same direction as TSR over time. By examining rolling three- and five-year periods over the past decade, we have identified financial measures that have a relatively strong positive correlation to TSR. However, since there are many company-specific and macroeconomic factors that impact performance over time, these analyses are intended to provide a directional perspective and not be prescriptive.

Findings

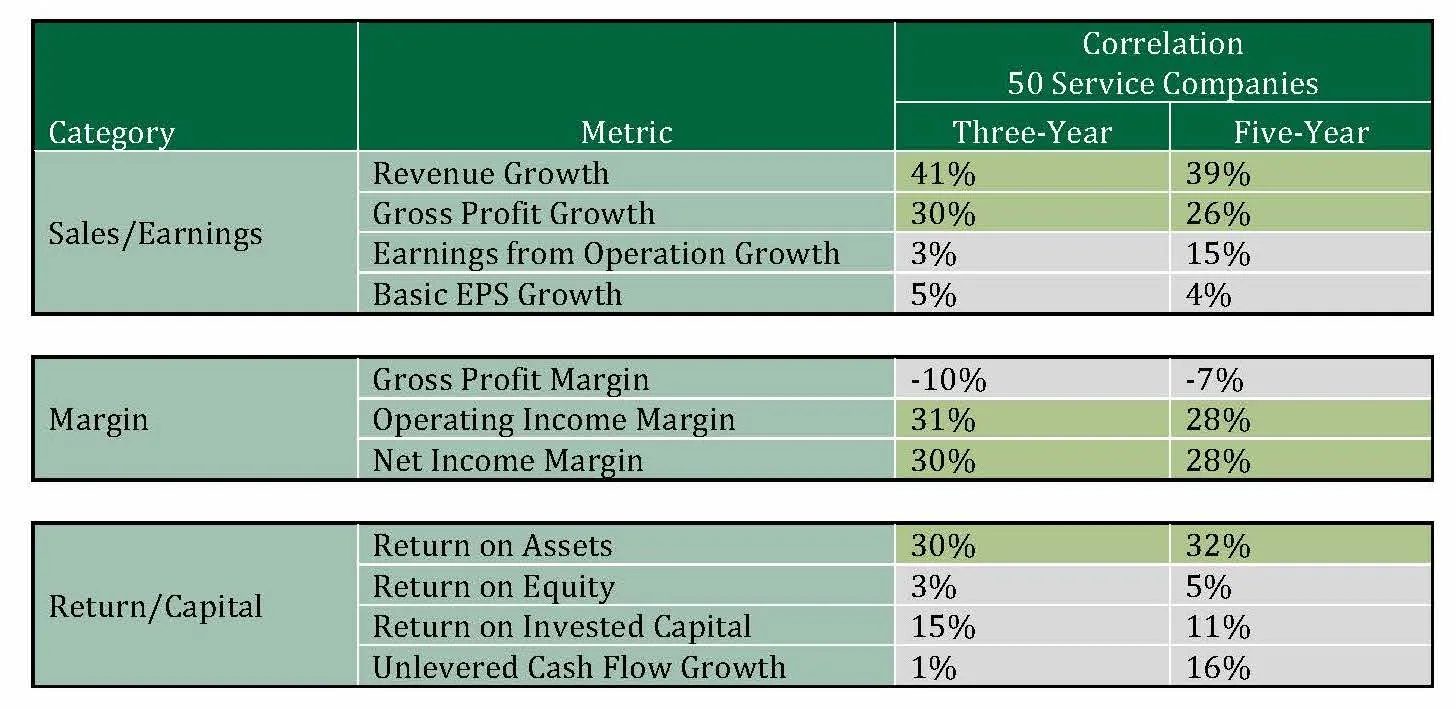

We analyzed 50 large manufacturing companies and found that the financial measures with the strongest correlation to TSR were: return on invested capital, operating income margin and net income margin. For a group of 50 service companies, we found that revenue growth had the strongest correlation with TSR, followed by gross profit, operating income margin, net income margin and return on assets.

Key Inputs

There are several key inputs when conducting TSR correlation analyses. For our illustrative analyses, we utilized the following inputs:

Measures – Sample of financial performance measures spanning the income statement, balance sheet, and cash flow statement. If a standardized database is used, the financial measure definitions will often vary from the specific incentive plan measures used by a company, which typically include certain adjustments.

Comparisons – Change in dollar amounts for income statement measures and the absolute margin or return level for percent-denominated measures.

Time period – Three- and five-year rolling time periods over 10 years (ending in 2017).

Correlation strength – Relatively stronger correlations were defined as being ≥25%.

Example Output

The charts below illustrate the correlation of various financial metrics with TSR over three- and five-year periods. Metrics with correlations of ≥25% are highlighted in green. Financial performance data reflect standardized definitions provided by S&P Capital IQ (they have not been customized or adjusted).

Table A: Industrial Company Metric Correlation Analysis withTSR (50 companies)

Table B: Service Company Metric Correlation Analysis withTSR (50 companies)

Closing

TSR correlation analysis provides companies with another perspective as they confirm or reevaluate the appropriateness of their incentive plan performance measures. Due to certain limitations, including the use of historical data at various points in time and the uniqueness of individual companies in a given peer set, TSR correlation analysis should be considered directional. A general correlation analysis, as illustrated here, is a starting point. As a next step, a company may decide that further refinement is warranted in order to determine the most appropriate form of the metric to be used (i.e., “underlying earnings”). In the end, companies should select incentive plan performance measures that best align to their business strategy to drive long-term shareholder value.