The Stakeholder Model and ESG

Introduction

In August 2019, the Business Roundtable (BRT) released its new stakeholder model of the revised purpose of the corporation, stating explicitly that businesses exist to serve multiple stakeholders ” including customers, employees, communities, the environment, and suppliers ” in addition to shareholders.[i] This new model was publicly supported by 181 CEOs of major corporations. It could have a substantial impact on corporate incentive designs, metrics, and other governance areas as corporations continue or begin to operationalize this stakeholder model into their long-term strategies, as incentive plans are core to reinforcing and communicating business strategy. While there are many opinions on the BRT statement, the stakeholder model is evolving in both importance and sophistication.[ii]

Further, the COVID-19 pandemic, the associated economic impacts, and increased focus on social justice illustrate the increasing expectations on ” and willingness of ” corporate leaders to address social issues that may extend beyond a traditionally narrower view of the business purpose of the corporation. Given these circumstances, some companies are taking a fresh look at their impact on numerous stakeholder groups and their reinforcing impact on company success. For example: Will increased focus on employee wellness initiatives enhance the resilience of corporations? Will sustainable supply chains and real estate differentiate a company in both the consumer and talent markets, or are these practices rapidly becoming baseline expectations of employees, investors, customers, and the broader community? The answers to these questions are beyond the scope of our expertise, but these and similar questions are at the center of the discussion on ESG metrics and their applicability to incentive compensation.

If the stakeholder model represents an emerging model for the strategic vision of a company, ESG (Environmental, Social, and Governance) metrics can be used to assess and measure company performance and its relative positioning on a range of topics relevant to the broader set of company stakeholders in the same way that financial metrics assess company performance for shareholders. This Viewpoint will address, at a “conceptual” level, key questions and guidelines for assessing a company’s readiness for ” and potential approach to ” implementing ESG metrics and goals in executive incentive programs. We are applying our significant expertise in the design of executive incentive programs to the emerging paradigm of ESG-focused goals in the context of the evolving stakeholder model.

Background

The BRT statement drew significant interest from the press and corporate governance community as it was viewed by many ” some investors, the media, academics, and some legal commentators [iii] ” as a social and economic enhancement to, or replacement of, the concept of “shareholder primacy” as popularized by Milton Friedman and supported by many institutional investors and their advisors.[iv] Others viewed it as a contradiction to, or a distraction from, the very successful shareholder model which has created prosperity over decades for shareholders and many other stakeholders.[v]

Pragmatically, the BRT’s statement may be a continued evolution of corporate culture and strategy that seeks to place more direct focus on the role that stakeholders have long played in the corporation from the corporate governance, management, and board perspectives. This sentiment is reflected in the member quotes included in the BRT’s release as well as a recent Fortune CEO survey in which a majority of CEOs surveyed (63%) “…agree with the [BRT’s] statement and believe most good companies always have operated that way.”[i] ,[vi] In this context, the BRT’s statement serves to enhance, clarify, and substantially debate the sometimes-counterproductive dichotomy of “stakeholders versus shareholders.” ESG metrics, applied to this clarified purpose of the corporation, provide the quantifiable and generally accepted means to measure this more nuanced view of company performance.

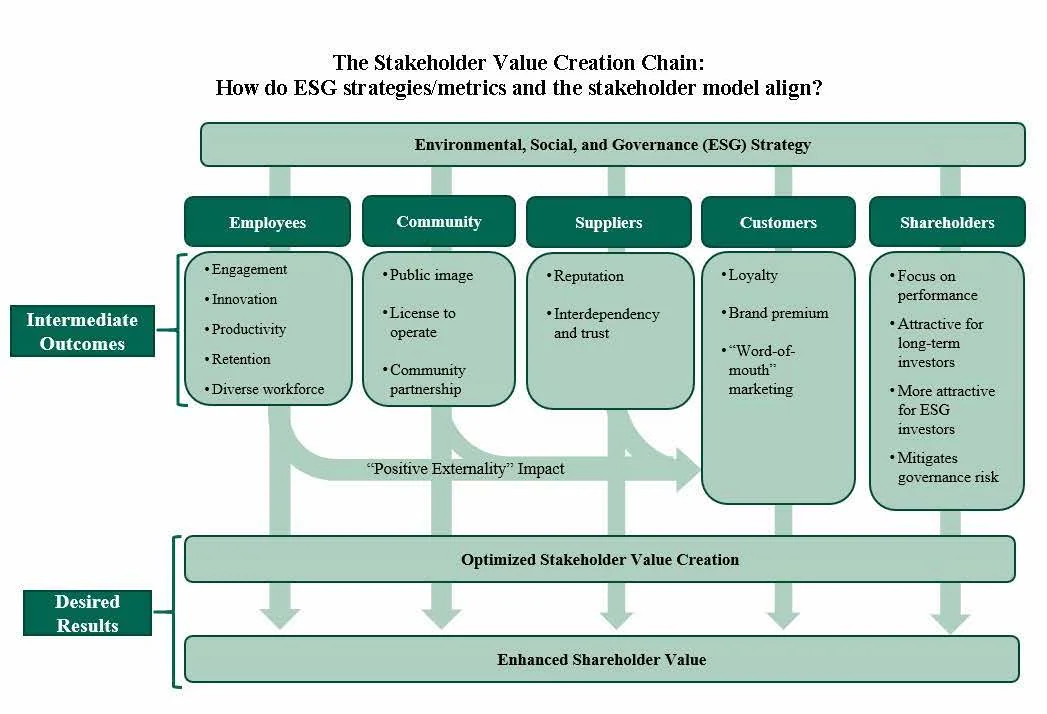

The “Stakeholder Value Creation Chain” below is a model developed by Pay Governance to illustrate the intersection of ESG strategy, the stakeholder model, and the creation of firm value. The model captures the reinforcing carryover effect of stakeholders’ contributions to the economic success of the company. An example of a “positive externality” is that many employees want to work for environmentally friendly companies, and the increased engagement of those employees may also increase productivity, customer satisfaction, etc. All companies need to balance their stakeholders’, including shareholders’, long-term interests. It may be a greater challenge for economically stressed companies to make long-term investments for other stakeholders than it is for top-performing companies to do so. However, our research and others’ find that, overall, companies manage both short- and long-term performance trade-offs efficiently. [vii], [viii] These findings support optimistic outcomes for this Stakeholder Value Creation Chain.

These developments, and interest in this model of value creation generally, have prompted an increase in questions about whether and how to include ESG metrics in incentive plans. Below, we provide some key questions and guidelines for assessing a company’s readiness and potential approach for implementing ESG metrics in executive compensation incentive programs.

Is your company ready to set or disclose ESG incentive goals?

ESG incentive metrics are like any other incentive metric: they should support and reinforce strategy rather than lead it. Companies considering ESG incentive metrics should align planning with the company’s social responsibility and environmental strategies, reporting, and goals. Another essential factor in determining readiness is the measurability/quantification of the specific ESG issue.

Companies will generally fall along a spectrum of readiness to consider adopting and disclosing ESG incentive metrics and goals:

1) Companies Ready to Set Quantitative ESG Goals: Companies with robust environmental, sustainability, and/or social responsibility strategies including quantifiable metrics and goals (e.g., carbon reduction goals, net zero carbon emissions commitments, Diversity and Inclusion metrics, employee and environmental safety metrics, customer satisfaction, etc.).

2) Companies Ready to Set Qualitative Goals: Companies with evolving formalized tracking and reporting but for which ESG matters have been identified as important factors to customers, employees, or other stakeholders. These companies likely already have plans or goals around ESG factors (e.g., LEED [Leadership in Energy and Environmental Design]-certified office space, Diversity and Inclusion initiatives, renewable power and emissions goals, etc.).

3) Companies Developing an ESG Strategy: Some companies are at an early stage of developing overall ESG/stakeholder strategies. These companies may be best served to focus on developing a strategy for environmental and social impact before considering linking incentive pay to these priorities.

We note it is critically important that these ESG/stakeholder metrics and goals be chosen and set with rigor in the same manner as financial metrics to ensure that the attainment of the ESG goals will enhance stakeholder value and not serve simply as “window dressing” or “greenwashing.” [ix] Implementing ESG metrics is a company-specific design process. For example, some companies may choose to implement qualitative ESG incentive goals even if they have rigorous ESG factor data and reporting.

Will ESG metrics and goals contribute to the company’s value-creation?

The business case for using ESG incentive metrics is to provide line-of-sight for the management team to drive the implementation of initiatives that create significant differentiated value for the company or align with current or emerging stakeholder expectations. Companies must first assess which metrics or initiatives will most benefit the company’s business and for which stakeholders. They must also develop challenging goals for these metrics to increase the likelihood of overall value creation. For example:

- Employees: Are employees and the competitive talent market driving the need for differentiated environmental or social initiatives? Will initiatives related to overall company sustainability (building sustainability, renewable energy use, net zero carbon emissions) contribute to the company being a “best in class” employer? Diversity and inclusion and pay equity initiatives have company and social benefits, such as ensuring fair and equitable opportunities to participate and thrive in the corporate system.

- Customers: Are customer preferences driving the need to differentiate on sustainable supply chains, social justice initiatives, and/or the product/company’s environmental footprint?

- Long-Term Sustainability: Are long-term macro environmental factors (carbon emissions, carbon intensity of product, etc.) critical to the Company’s ability to operate in the long term?

- Brand Image: Does a company want to be viewed by all constituencies, including those with no direct economic linkage, as a positive social and economic contributor to society?

There is no one-size-fits-all approach to ESG metrics, and companies fall across a spectrum of needs and drivers that affect the type of ESG factors that are relevant to short- and long-term business value depending on scale, industry, and stakeholder drivers. Most companies have addressed, or will need to address, how to implement ESG/stakeholder considerations in their operating strategy.

Conceptual Design Parameters for Structuring Incentive Goals

For those companies moving to implement stakeholder/ESG incentive goals for the first time, the design parameters range widely, which is not different than the design process for implementing any incentive metric. For these companies, considering the following questions can help move the prospect of an ESG incentive metric from an idea to a tangible goal with the potential to create value for the company:

1) Quantitative goals versus qualitative milestones. The availability and quality of data from sustainability or social responsibility reports will generally determine whether a company can set a defined quantitative goal. For other companies, lack of available ESG data/goals or the company’s specific pay philosophy may mean ESG initiatives are best measured by setting annual milestones tailored to selected goals.

2) Selecting metrics aligned with value creation. Unlike financial metrics, for which robust statistical analyses can help guide the metric selection process (e.g., financial correlation analysis), the link between ESG metrics and company value creation is more nuanced and significantly impacted by industry, operating model, customer and employee perceptions and preferences, etc. Given this, companies should generally apply a principles-based approach to assess the most appropriate metrics for the company as a whole (e.g., assessing significance to the organization, measurability, achievability, etc.) Appendix 1 provides a list of common ESG metrics with illustrative mapping to typical stakeholder impact.

3) Determining employee participation. Generally, stakeholder/ESG-focused metrics would be implemented for officer/executive level roles, as this is the employee group that sets company-wide policy impacting the achievement of quantitative ESG goals or qualitative milestones. Alternatively, some companies may choose to implement firm-wide ESG incentive metrics to reinforce the positive employee engagement benefits of the company’s ESG strategy or to drive a whole-team approach to achieving goals.

4) Determining the range of metric weightings for stakeholder/ESG goals. Historically, US companies with existing environmental, employee safety, and customer service goals as well as other stakeholder metrics have been concentrated in the extractive, industrial, and utility industries; metric weightings on these goals have ranged from 5% to 20% of annual incentive scorecards. We expect that this weighting range would continue to apply, with the remaining 80%+ of annual incentive weighting focused on financial metrics. Further, we expect that proxy advisors and shareholders may react adversely to non-financial metrics weighted more than 10% to 20% of annual incentive scorecards.

5) Considering whether to implement stakeholder/ESG goals in annual versus long-term incentive plans. As noted above, most ESG incentive goals to date have been implemented as weighted metrics in balanced scorecard annual incentive plans for several reasons. However, we have observed increased discussion of whether some goals (particularly greenhouse gas emission goals) may be better suited to long-term incentives. [x] There is no right answer to this question ” some milestone and quantitative goals are best set on an annual basis given emerging industry, technology, and company developments; other companies may have a robust long-term plan for which longer-term incentives are a better fit.

6) Considering how to operationalize ESG metrics into long-term plans. For companies determining that sustainability or social responsibility goals fit best into the framework of a long-term incentive, those companies will need to consider which vehicles are best to incentivize achievement of strategically important ESG goals. While companies may choose to dedicate a portion of a 3-year performance share unit plan to an ESG metric (e.g., weighting a plan 40% relative total shareholder return [TSR], 40% revenue growth, and 20% greenhouse gas reduction), there may be concerns for shareholders and/or participants in diluting the financial and shareholder-value focus of these incentives. As an alternative, companies could grant performance restricted stock units, vesting at the end of a period of time (e.g., 3 or 4 years) contingent upon achievement of a long-term, rigorous ESG performance milestone. This approach would not “dilute” the percentage of relative TSR and financial-based long-term incentives, which will remain important to shareholders and proxy advisors.

Conclusion

As priorities of stakeholders continue to evolve, and addressing these becomes a strategic imperative, companies may look to include some stakeholder metrics in their compensation programs to emphasize these priorities. As companies and Compensation Committees discuss stakeholder and ESG-focused incentive metrics, each organization must consider its unique industry environment, business model, and cultural context. We interpret the BRT’s updated statement of business purpose as a more nuanced perspective on how to create value for all stakeholders, inclusive of shareholders. While optimizing profits will remain the business purpose of corporations, the BRT’s statement provides support for prioritizing the needs of all stakeholders in driving long-term, sustainable success for the business. For some companies, implementing incentive metrics aligned with this broader context can be an important tool to drive these efforts in both the short and long term. That said, appropriate timing, design, and communication will be critical to ensure effective implementation.

Appendix 1: Mapping the Intersection of ESG Metrics and Stakeholder Impact

According to a recent Bank of New York Mellon survey, some the most prevalent questions from investors fielded by corporate investor relations professionals surveyed concern board composition and structure, diversity and inclusion, climate change and carbon emissions, executive compensation, and energy efficiency.[xi]

The illustrative table below provides Pay Governance’s generalized perspective on the alignment between ESG initiatives and the directly impacted stakeholders. The matrix below is illustrative and is not exhaustive of all ESG metrics and stakeholder impacts.

References

____________________________________